Summary: Markets settled in Asia and Europe following Wall Street’s rout as China pledged to start delivering upon trade agreements with the US. American stock futures rose even as their markets will close today to remember the life of ex-President George H.W. Bush.

The Dollar edged up in quiet trading. Weaker-than-forecast third quarter GDP weighed on the Australian Dollar which slumped 1.09%. The Euro was little-changed even as Italian bonds rallied on optimism for a positive end to its budget dispute with the European Union. Canada’s Loonie fell 0.95% even as the Bank of Canada left its benchmark rate unchanged at 1.75%. The Bank of Canada saw economic momentum waning for the fourth quarter this year.

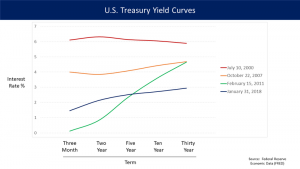

Global bond yields steadied. The benchmark US 10-year treasury yield was unchanged at 2.91%.

- The US S&P 500 bounced off its low at 2698 to close at 2718, up 0.6%. The latest Federal Reserve’s Beige Book report, released at the NY close today, showed modest growth in the economy. The report is consistent with the expectations that the Fed will only gradually raise interest rates and buoyed Wall Street stock futures.

- USD/JPY – rallied 0.45% to close at 113.18 from 112.80 at the close yesterday. The Dollar held steady together with the US bond yields. The yield on Japan’s 10-year JGB closed flat at 0.06%. The recent 112.60-113.60 looks set to continue for now. The speculative market remains short of Yen and this should limit the topside of USD/JPY.

- EUR/USD – finished the day flat at 1.1340. The multi-currency is having difficulty making a decisive move either way and had a relatively quiet trading range of 50 pips. Euro-area services PMI were mostly flat as pointing to moderate GDP growth in the region. EUR/USD has traded between 1.1300 and 1.1420 for a week now. We can expect more of the same with the impetus to come from tomorrows US Payrolls and Wages number.

- AUD/USD – after a strong rally in the past week to a high of 0.7393, the Aussie slumped back under 0.73 cents to close at 0.7268 last night. Australia’s growth in the third quarter printed weaker-than-expected at 0.3% against a forecast of 0.6% and Q2’s 0.9%. A rise in China’s Caixin Services PMI in November steadied the Aussie.

On the Lookout: With the US markets out today to remember the life of ex-President George H.W. Bush, trading conditions should stay relatively quiet. The established ranges on the ‘majors’ against the USD will stay intact, for now. Emerging Market currencies were stable with moves contained. Today’s data sees Australia’s Retail Sales and Trade Balance for November, Germany’s Factory Orders and the US Weekly Jobless Claims and Factory Orders. US Federal Reserve Chairman Jerome Powell is due to speak on the economy to a Housing Council’s annual event in Washington DC (9.30 am, Dec 7 Friday in Sydney). Finally, tomorrow is Friday US Payrolls Day with Wages the clear focus.

Trading Perspective:

- AUD/USD – the Aussie was pummelled on the dismal Q3 GDP data. The steam out of the recent rally has evaporated and we can expect some downside tests. AUD/USD was trading around the 0.7345 level when the data was released. Traders sold the Aussie down to 0.7285 where it steadied before further selling saw a low of 0.7260. We can expect support at the 0.7260 level to hold first up. Further support lies at 0.7220. Resistance is found at 0.7300. Look for a trading range today of 0.7230-0.7280. The latest CFTC report saw net speculative AUD shorts pared to -AUD 53,903 contracts. Still a decent number of shorts.

- EUR/USD – should hold the 1.1310 lows last night with a probable range today of 1.1310-1.1370. Yesterday Italian Deputy PM Luigi Di Miao noted that the climate was changing in its budget talks with the European Union. Di Miao reiterated that Italy wants to avoid any disciplinary action from the EU. The yield on Germany’s 10-year Bund rose one basis point to 0.27%.

- USD/JPY – The Dollar rallied from 112.65 lows to a high of 113.24 this morning before settling at the close at 113.18. One of the key themes for 2019 is that of monetary policy convergence. Global central banks, including the BOJ will follow the path of the US Fed in removing accommodative policy stances and gradually raising interest rates. In July this year the BOJ introduced monetary policy adjustments and allowed a wider trading range for Japanese Government Bonds (JGB’s). The market believes that the BOJ will continue with its ultra-loose monetary policy. Speculative trades have been to increase short JPY bets. This number has grown to -JPY 104,324 from +JPY 5,000 in June 2018. USD/JPY has ranged between 110.40 and 113.80 since then. For today, look for further consolidation with a likely range of 112.75-113.35.

- USD/CAD – The US Dollar closed up 0.97% against the Loonie at 1.3385 (1.3255 yesterday). The Bank of Canada left its benchmark interest rate unchanged at 1.75%. In late October the BOC raised its rate and indicated that rates would need to rise to keep inflation in check. Since then global oil prices have experienced a steep decline and this has impacted Canada’s energy sector, a big driver for their economy. Speculators are modestly short Canadian Dollars from the latest CFTC report (-CAD 8,630 contracts). The 1.3400 level is strong resistance and it’s hard to see a clean break of that just now unless the US Dollar should strengthen considerably.