Asian stocks finished strong as investors cheered progress in trade negotiations between the US and China in Beijing. In Japan, the Nikkei225 main index added 0,82 percent to 21,205, the Hang Seng benchmark in Hong Kong finished 0.99 percent higher at 29,060. The Shanghai Composite outperformed, finishing 3.20 percent higher at 3,090 and in Singapore, the FTSE Straits Times index gained 0.46 percent higher at 3,218. Australian equities are also in positive performance. The ASX 200 however lost some earlier gains to close up 4 points or 0.1% to 6,180. Over the first three months of the year, the Aussie market rallied 9.5% — marking the best start to the year since 1991.

In commodities markets, Light Crude Oil started strong the session and trades at 59.61, while Brent oil is trading lower at $67.33/barrel. The Energy Information Administration data released yesterday showed that domestic crude stocks rose by 2.8 million barrels per day during the week ended March 22, bringing the figure to 442.3 million barrels, which reportedly amounts to a 3% increase year-on-year. Gold lost over 20 dollars yesterday to three-week lows and broke below the $1300 and the 50-day moving average at $1306 amid stronger Greenback. XAUUSD technical picture has deteriorated, and now immediate support stands at 100-day moving average at $1277, which can accelerate the downward move down to new YTD lows at the 200-day moving average at $1247. Strong resistance now stands at the $1300 round figure.

A positive start for equities in early European session mirroring the improved sentiment in Asian markets as investors watching the developments surrounding Brexit, DAX30 gains 0.32 percent to 11,465. CAC40 is 0.58 percent higher at 5,327 while FTSE100 in London is 0.44 higher at 7,266 and the FTSE MIB in Milan is trading 0.31 percent higher at 21,110.

On the Lookout: The Mexico Central bank board voted to hold rates at 8.25% as the balance of risk remains to be tilted to the downside.

In US macro news and according to the Department of Commerce’s third estimate for fourth-quarter gross domestic product, the US economy expanded at a quarterly annualised pace of 2.2% over the three months to December, down from 3.4% in the previous quarter and versus a previous estimate of 2.6%. Figures from the National Association of Realtors were also weaker than expected, with the NAR’s monthly index down 1% from January to 101.9 last month versus expectations for a 0.5% drop.

In our calendar today the highlight is likely to be the preliminary March CPI releases in France, Italy, and the Euro-area along with the release of January Core PCE data in the US and final 4Q GDP in the UK and Spain. Besides, we will also be getting France’s February YTD budget balance and Feb consumer spending data, Germany’s March employment report, Italy’s February PPI and the UK’s February consumer credit, money supply, and mortgage approvals data. In the US, we will get the February personal income, personal spending, and new home sales data along with March Chicago purchasing manager index and final March University of Michigan survey results.

Key Upcoming Events

10/04/2019 ECB Interest Rate Decision

12/04/2019 UK leaves the European Union

18/04/2019 Dissolvement of current EU Parliament

Trading Perspective: In forex markets, AUDUSD is under selling pressure below 0.71 as traders digest the latest disappointing data from the Aussie economy. Kiwi, trying to stabilize at the lows from the recent sell-off at 67.90, after the Reserve Bank of New Zealand (RBNZ) abandoned its long-standing neutral stance and turned dovish, saying that the next move in interest rates would likely be down. US dollar index is losing some pips and now is trading at 96.38 after capped in the 96.80 region in the wake of the dovish FOMC event last week.

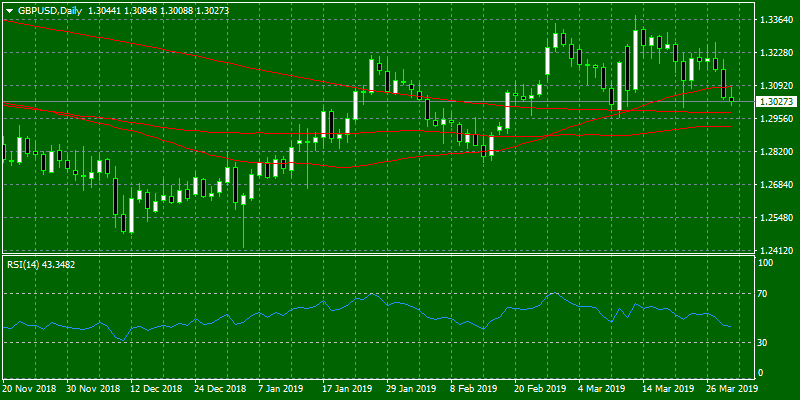

GBPUSD investors turn bearish for the first time in March as the pair broke below the 50-day moving average awaiting new votes related to Brexit from the Parliament. On the downside, major support will be found at 1.30 round figure while more protection can be found at the 200-day moving average around 1.2980. On the flip side, immediate resistance stands at 1.3088 the high from Asian session, and from there major resistance can be found at 1.3202 where the 50-hourly moving average stands and then at 1.3232 the cross point of 100 and 200-hourly moving averages while 1.3382 the yearly high will be met with strong supply.

In GBP futures markets open interest increased by almost 5.4K contracts on Thursday from Wednesday’s final 143,396 contracts. On the other hand, volume reversed the previous build and dropped by nearly 9.2K contracts.

EURUSD broke below the strong horizontal lower band of the short term trading range, and now an attempt to 1.12 looks possible before a move to test YTD low at 1.1180. The pair looks vulnerable and fails to make any rebound on worse US economic news. 1.1244, the 50-hour moving average is a level that the pair must recapture in order to attract some bids.

On the Euro political front, headwinds are expected to emerge in light of the upcoming EU parliamentary elections, where the focus of attention will be on the potential increase of the populist and right-wing option among voters.

In Euro futures markets, traders added around 2K contracts to their open interest positions on Thursday, while volume shrunk by nearly 22.3K contracts after two consecutive daily builds.

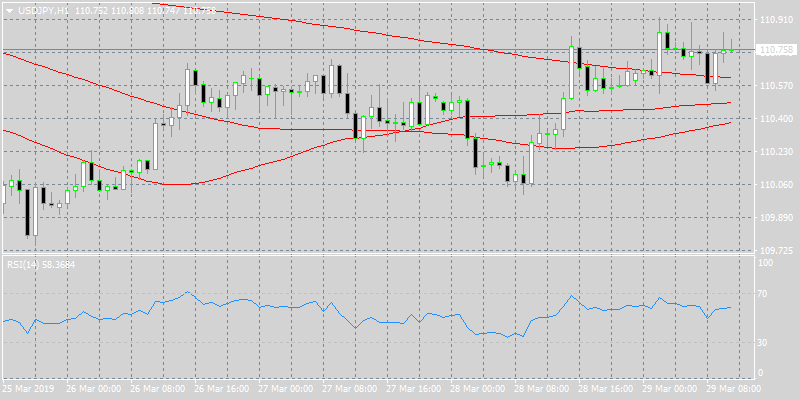

USDJPY gains momentum and trades at the daily high to 110,80 zone having hit the low at 110.52. Major support for the pair stands at 110 round figure. Immediate resistance for the pair stands at the 111 round mark and then at the 111.19 where the 100-day moving average crosses, followed by 111.49 the 200-day moving average stands.

Open interest in JPY futures markets rose by just 363 contracts on Thursday and volume rose for the second session in a row, this time by 483 contracts.