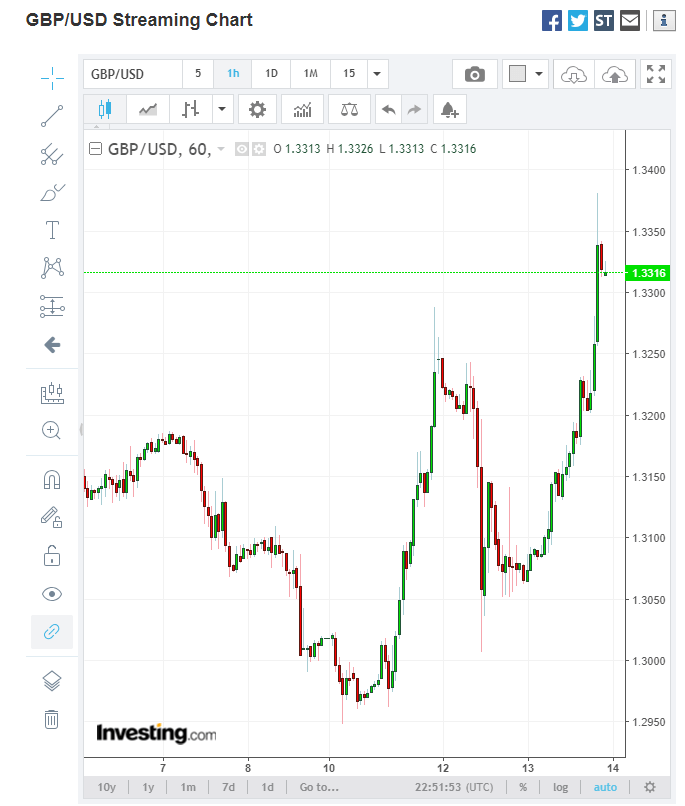

Summary: Sterling once again took centre stage in the FX markets, soaring over 2% after the UK Parliament rejected a NO-Deal Brexit. The British Pound spiked in early Sydney to 1.3381 following its NY close of 1.3248 in choppy trade. The result paves the way for a vote to delay Brexit. Despite the political chaos and uncertainty in the UK, the British Pound remains strong.

US Headline and Core PPI in February missed forecasts, rising 0.1% (vs f/c 0.2%). This was the weakest annual increase in 18 months. The Dollar extended losses against it’s major rivals. EUR/USD hit one-week highs, climbing to 1.13386 before settling at 1.1325. The Australian Dollar lifted to 0.7097 despite a weak Westpac consumer confidence report.

Wall Street stocks rallied on optimism generated by the UK vote against a NO-Deal Brexit. The DOW finished 0.5% up at 25,700 (25,552. Yesterday). The benchmark US 10-year bond yield stabilised, up one-basis point to 2.61%.

- GBP/USD – The British currency jumped to fresh 8-month highs in early trade to 1.3381 before settling at 1.3325 currently. Sterling reversed losses yesterday at 1.3080 climbing to 1.3260 before the Parliament vote were a rejection was expected. The rejection of a NO-Deal Brexit now moves to a vote to delay.

- EUR/USD – The Single currency benefited from Sterling’s rally although the EUR/GBP cross slumped to near two-year lows. The EUR/USD finished up 0.42% at 1.1333 in New York.

- AUD/USD – the Australian Dollar grinded higher on the back of a generally softer US Dollar. The Aussie Battler rallied to 0.7097 before settling at 0.7093 (0.7085 yesterday). Westpac’s Consumer Sentiment Index fell to -4.8% to 98.8, the weakest reading since late 2017.

On the Lookout: So far, US economic data in February has been weaker than expected. Friday’s big US Jobs Creation miss was followed by modestly lower consumer and producer prices. Still the data has not been dramatic enough to change the Fed’s patient, “wait-and-see” approach to any rate increases this year.

Today the focus moves to China where the trifecta of Industrial Production, Retail Sales (both January) and Fixed Asset Investment (February) data are released later this morning. Germany and France release their February Final CPI report (m/m and y/y). The US rounds today’s data off with New Home Sales (Feb), Weekly Unemployment Claims and Import Prices.

Trading Perspective: The Dollar has edged lower this week on weaker-than-expected US economic data and falling yields. So far, the move has been corrective given the market’s long US Dollar positioning. The Dollar Index (USD/DXY) has dropped from 97.70 highs last week to 96.49 this morning. US bond yields stabilised yesterday. The 10-year yield rose to 2.61% (2.60%). Two-year US bond yields closed at 2.46% (2.45%). Expect some consolidation with more two-way trade today. The Dollar Index (USD/DXY) should find solid support at current levels (96.40/50). The UK still faces much uncertainty over Brexit which should see the Pound ease from current levels.

- GBP/USD – the spike to 1.3381 this morning occurred in thin, low-volume early trade. It smacks of a large stop triggered above 1.3320. The big test comes later in the European day when Parliament votes again on what type of extension and the support it gets from the Euro bloc’s 27 members. GBP/USD currently trades at 1.3315. Immediate resistance can be found at 1.3340 and 1.3380. Immediate support lies at 1.3270 and 1.3240. Look for further choppy trade where the risk from current levels is lower.

- EUR/USD – The Euro traded to a high of 1.1339 overnight. The resistance level at 1.1340 is strong. EUR/USD would need a sustained break of the 1.1340 resistance to push it higher. The next resistance level comes in at 1.1360-70. Immediate support can be found at 1.1300 followed by 1.1270. Look for consolidation with a likely trade today between 1.1270 and 1.1340. The Euro is not quite out of the woods yet, but the market remains short.

- AUD/USD – The Aussie’s rally fell short of 0.7100 which is today’s immediate resistance level. The next resistance level lies at 0.7130/40. Immediate support for the Aussie Battler can be found at 0.7070 and 0.7040. Despite the much weaker than expected Westpac Consumer Confidence report the Aussie remains stable. An overall weaker US Dollar and a short Aussie market have lifted the antipodean currency. Look for consolidation as traders await today’s trifecta of Chinese data. Likely range 0.7050-0.7100. Just trade the range shag on this one.

- USD/JPY – The Dollar has been remarkably stable against the Yen given its moves against its other Rivals. Traders expect the Bank of Japan to downgrade its economic outlook in tomorrows rates policy meeting. USD/JPY traded to 111.46 highs overnight before settling at 111.13 this morning. Immediate resistance can be found at 111.40/50 followed by 111.80. Immediate support lies at 111.00 (overnight lows) and 110.70. For today we can expect a trading range between 110.90-111.50. Prefer to sell rallies as the market positioning is still long USD/JPY.

- USD/DXY – The Dollar Index closed just above strong support at 96.40. It has dropped from 97.70 to its current 96.486 in a week’s time. The next support level lies at 96.20. Immediate resistance can be found at 96.80 and 97.10. With US yields stabilising expect the support at 96.40 to hold within a range today of 96.45-96.85.

Happy trading all.