Summary: China’s central bank, the PBOC, took steps yesterday to strengthen the Yuan after it weakened through the psychological 7 per Dollar level. The People’s Bank of China fixed the official daily reference to 6.9683, below the key 7 rate. The Dollar had rocketed against the Chinese currency to a 7.1390, its highest since 2008, on worsening trade relations with the US. Which sparked widespread risk aversion and a spike in currency volatility. Traditional havens, the Yen and Swiss Franc soared while the Australian Dollar, Risk and Emerging Market currencies (Russian Rouble, SA Rand) tumbled. The stronger Chinese Yuan saw a reversal of most of yesterday’s moves. USD/JPY reversed higher, finishing at 106.47 (106.05 yesterday) while USD/CHF was up 0.41% to 0.9765. The Dollar Index (USD/DXY) lifted to 97.571 from 97.380 while the Euro slipped 0.37% to 1.1205 (1.1225). The Australian Dollarsteadied to 0.6760 (0.6758). Sterling edged up to 1.2167 (1.2140). The New Zealand Dollar dipped to 0.6525 (0.6535) ahead of today’s RBNZ policy meeting where the Kiwi central bank is widely expected to trim its Overnight Cash Rate by 0.25%.

The rise in risk appetite lifted Wall Street. The DOW gained 1.6% to 25,972 (25,540). The S&P 500 finished 1.83% higher at 2.877. (2,825). US Treasury yields steadied with the benchmark 10-year rate at 7.0 % after it briefly broke through to 1.67%, its lowest since late 2016.

Brent Crude Oil prices slid 1.96% to US$ 58.55 on the ongoing trade tensions.

The RBA kept interest rates on hold as expected. Traders see another RBA rate cut at year-end.

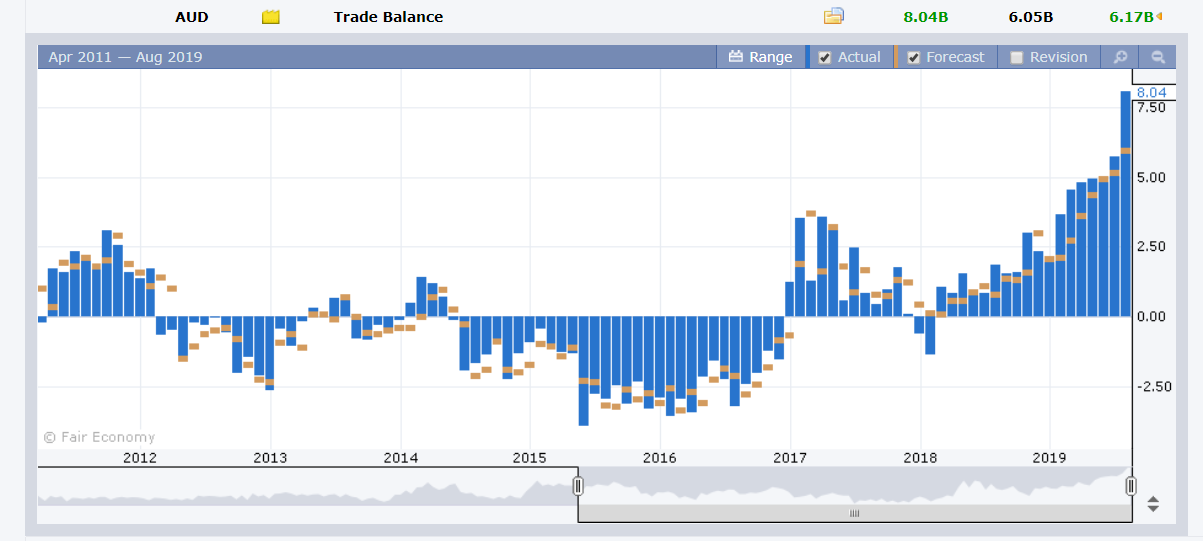

Data releases yesterday saw Australia’s Trade Surplus climb to AUD 8.04 billion, beating forecasts of AUD 6.05 billion. Japanese Household Spending outperformed rising 2.7% in July versus forecast of 1.3%. Germany’s July Factory Orders gained 2.5% beating expectations of 0.5%.

- USD/JPY – The Dollar rebounded to close at 106.45, off yesterday morning’s early lows at 105.52. The rally in risk appetite, steady US bond yields and Japanese corporate buying all combined to lift the Greenback against the haven-sought Yen.

- EUR/USD – The Single currency lost 0.37% to 1.1205 after opening at 1.1225 and trading to a high at 1.12496. Ten-year German Bund Yields slipped 2 basis points to -0.54%, which weighed on the Single Currency.

- AUD/USD – The Australian Battler rallied off it’s base at .6748 to 0.68008 after the PBOC Yuan fix lifted risk appetite. The RBA kept interest rates on hold as was widely expected. The rally in the US Dollar pushed the AUD/USD back down to close little changed at 0.6760.

On the Lookout: The recovery in risk remains languid and it will take more measures to keep it alive. Watch for the PBOC’s Yuan Fix today as well as comments from Chinese and US officials. St Louis Fed President and FOMC member James Bullard said yesterday that monetary policy cannot react to day-to-day trade headlines. Yesterday’s rapid deterioration in risk had traders forecasting a 0.5% Fed rate cut next month. The US Treasury Department announced that China had manipulated its currency, the first time since 1994. Markets will remain cautious with no end to the escalating trade conflict.

The RBNZ is widely expected to trim its Official Cash Rate to 1.25% from 1.5% at the conclusion of its policy meeting today (12.30 pm Sydney time). The New Zealand central bank has its rate statement and press conference shortly after.

Data releases today begin with the Euro area. Germany’s Industrial Production for July is followed by the French Trade Balance. The UK releases its Halifax House Price Index (July). US Consumer Credit report rounds up the day’s data releases. FOMC member and Chicago Fed President Charles Evans speaks at a function in Chicago.

Trading Perspective: Currency volatility is back. Traders would hope so. All eyes in Asia will be on the People’s Bank of China and where they fix the Yuan today.

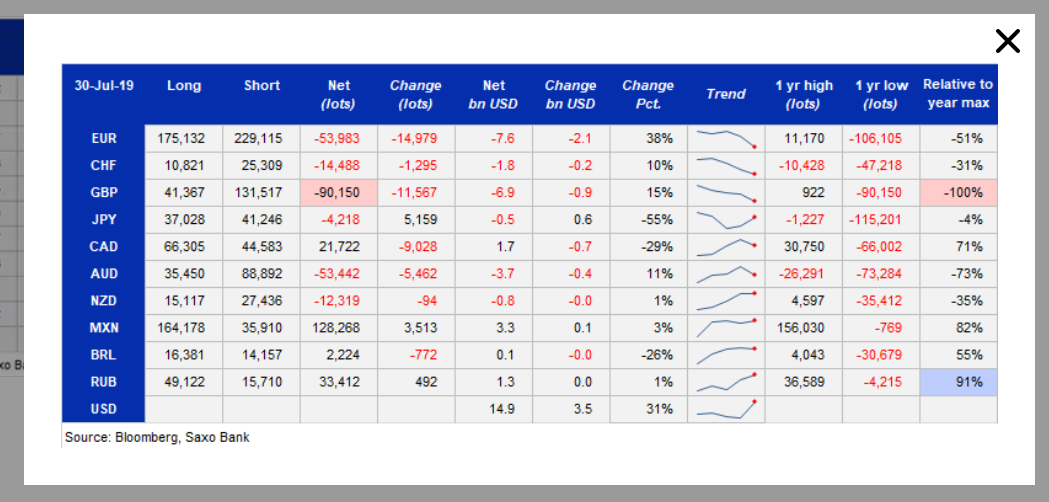

Meantime, the latest Commitment of Traders/CFTC report saw traders increase net US Dollar longs against the Pound, Euro, Aussie, Swiss and Canadian Dollar. The Yen was the only major currency where Dollar longs were trimmed. The Dollar still has room to trade lower.

- EUR/USD – The Euro closed around 1.1205 after trading to 1.12496 overnight and 3-week highs. The Single currency plummeted to 1.1027 on Friday last week. Expect consolidation at current levels with immediate resistance at 1.1250 to hold. Immediate support can be found at 1.1190 followed by 1.1150. The latest COT/CFTC report (week ended 30 July) saw net speculative Euro short bets increase to -EUR 53,983 contracts from the previous week’s

-EUR 39,004. Look to trade a likely range of 1.1185-1.1255 today. - GBP/USD – Sterling steadied to finish at 1.2168 from 1.2140 yesterday. Brexit fears were pushed aside with the focus on the China-US trade conflict. Last week the British currency was dumped by traders to 1.2080. Sterling traded to an overnight and one week high at 1.2210 before easing lower. GBP/USD has immediate resistance at 1.2200 and 1.2240. Immediate support lies at 1.2130 and 1.2100. The latest COT/CFTC report saw net speculative GBP shorts increase to -GBP 90,150 contracts from the previous -GBP 78,583. Total net shorts are now at multi-year highs. Look for a likely trading range today of 1.2140-1.2240. Prefer to buy dips.

- AUD/USD – The Aussie Battler has been battered of late. Australia’s trade relationship with China has weighed heavily on the currency as has the 2 RBA rate cuts in a row the past two months. The currency is now poised for a strong rally if the US Dollar continues to head south. Immediate resistance lies at 0.6800 and 0.6850. There is immediate support found at 0.6740 and 0.6710. The latest COT/CFTC report (week ended 30 July) saw speculative Aussie short bets increase to -AUD 53,442 contracts from -AUD 47,980. Look to buy dips with a likely range of 0.6740 to 0.6840. With the Aussie near lows against the US Dollar and on a Trade Weighted Basis, it’s a buy on dips. Australian data is also on the improve.

- USD/JPY – The Dollar slid against the Yen to a fresh 2019 low at 105.52 yesterday. The strong bounce and verbal intervention by the BOJ suggest that the 105.00 level will be supported for the time being by Japan Inc. USD/JPY rallied back to 107.087 overnight as some good old volatility came back to USD/JPY trading. The latest COT/CFTC report saw net speculative JPY trimmed to -JPY 4,218 contracts from -JPY 9,377. Which is the only major currency that saw a reduction. JPY shorts are at their smallest in a year. Immediate support today lies at 106.10 followed by 105.70. Immediate resistance can be found at 107.00 and 107.50. Look to buy dips with a likely range of 106.20-107.20.

Happy trading all.