Summary: The Dollar Index (USD/DXY), a measure of the value of the US Dollar relative to a basket of foreign currencies, slipped following disappointing US Payrolls data. A total of 155,000 jobs were created by the US economy in November, missing expectations of 196,000. October’s job gains were revised lower. The Unemployment rate remained unchanged at 3.7%, a 49-year low. November Wages data missed forecasts at 0.2% from 0.3%. The Euro eked out a 0.2% gain to finish around 1.1400. Interest rate futures revealed traders saw just one Fed rate increase in 2019.

Wall Street stocks slumped with the DOW ending 2.07% lower as investors kept a risk-off stance.

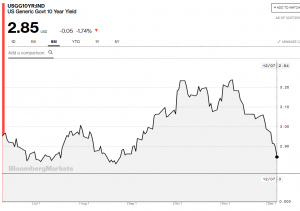

Global bond yields fell after stabilising on Thursday. The benchmark Ten-year US bond yield was 2 basis points lower to 2.85%.

T.Yield

- EUR/USD – the multi-currency closed at 1.1402, up 0.2% from Friday’s 1.1380. The Euro rose to an overnight high of 1.14235, before settling to close a touch lower. EUR/USD has failed to break its overall range of 1.1320 and 1.1420 since November 28. Traders will be looking at this week’s ECB meeting on Thursday to see if any breaks can be made.

- USD/JPY – little-changed, this currency pair closed at 112.68 from 112.58 Friday. The Dollar traded in a narrow range between 112.553 and 112.926, which is rare considering the Payrolls data release and the moves in the share markets. With the US 10-year yield slipping another 2 basis points lower, the pressure remains on the downside of Dollar-Yen.

- AUD/USD – against the trend, the Aussie fell further following it strong rally to just under 0.74 cents last week. AUD/USD closed at 0.7200, 0.7% lower than Thursday’s 0.7270. The fall in risk appetite has dented the Aussie’s confidence. Australian bond yields have fallen faster than its global counterparts. The 10-year Australian bond yield closed at 2.44% on Friday from 2.60% a week ago.

- GBP/USD – slip-sliding away into Tuesday’s crucial UK parliamentary vote on Brexit. The Pound slumped 0.52% to 1.2735 at the close on Friday from 1.2785. Concerns grew on whether British PM May can win a majority for her Brexit deal on December 11, Tuesday. May pressed ahead with plans on the parliamentary vote on her Brexit deal despite growing odds her deal would be rejected.

On the Lookout – Chinese data reported on Saturday saw China’s trade surplus expand further in November to CNY 306 billion (USD 44.7 billion) from a previous CNY 234 billion (USD 34 billion) and a forecast of CNY 227 billion (USD 36.2 billion). This will add to further pressure on risk sentiment and global trade.

We face another busy week ahead data and event wise. Japanese Current Account, and Final Q3 GDP as well as UK November GDP, Manufacturing and Industrial Production, and Goods Trade Balance are released today. Tomorrow sees the crucial UK Parliamentary vote on Brexit. US Headline and Core PPI are also due on Tuesday. Wednesday sees US inflation numbers out with Headline and Core CPI data for November. The Swiss National Bank and European Central Bank have their monetary policy meet decisions Thursday. On Friday we finish the week with Euro-area Flash Manufacturing and Services PMI data as well as US Headline and Core Retail Sales for November. That’s a lot to chew on, and we should see some volatility. Happy days!

Trading Perspective:

- AUD/USD – This currency pair opens near it’s low at 0.7200 cents and feels heavy. A break of 0.7190 could see 0.7160 strong support. The big drop in Australian yields, as well as the recent dovish tone from RBA Governor Philip Lowe have taken a lot of steam out of the Aussie. That said, expect the 0.7160 region to hold as the US Dollar continues to run out of steam. Tomorrow’s Commitment of Traders report from the CFTC on speculative positioning should be of interest in all currencies. The last report had speculators holding on to their short Aussie bets. The total should have been pared somewhat in the Aussie’s recent run-up. Looking to buy the dip to the 0.7160 area for another test of 0.7390. Likely range today 0.7170-0.7250.

- GBP/USD – Volatility is the name of the game for the British Pound. Traders will stay away from Sterling until they have a better sense of where Brexit is headed. The latest weekend news ahead of the parliamentary vote on Tuesday is looking like an inevitable failure. GBP/USD could be pushed down to as low as 1.2640, 2018 lows first up. For today immediate resistance lies at 1.2780/90. Get ready for more roller coaster rides in this currency pair. Likely range today 2650-1.2800.

- USD/JPY – the trading range has been narrowing up which suggest a break-through may be on the cards. Which is likely south for USD/JPY given the drop in the US 10-year bond yield. The last time the US 10-year yield was at 2.85% was in early September and USD/JPY was trading at 111.00. Look for a drift lower to 112.55 with a test of strong support at 112.20 likely. Immediate resistance can be found at 113.00.

- US Ten-year bond yield – There should be good support at 2.80/2.85 area. This week’s US inflation numbers will be closely watched by bond and interest rate futures traders. The topside though is coming lower, with 3.0% the limit.

Michael Moran

Michael Moran is an experienced global markets professional who currently writes a daily markets commentary. Moran has traded currencies for over 30 years, having worked in dealing rooms of major banks all over the globe. He lives in Sydney with his wife, 5 children, 2 grandsons and another coming. He still loves trading and talking about the currency markets. All of them! Michael began his career as an assistant dealer in money markets and foreign exchange with Lloyds Bank. He has worked in Hongkong, Manila, Tokyo, Singapore and Sydney. He’s traded through the 1985 Plaza Accord, Paul Keating’s 1986 “banana republic” statement, the Asian Currency Crisis in 1997, and the 9/11 New York Twin Tower terrorist strike. He took the task of speaking to sales team of the banks he worked at (Lloyds, NAB, CBA) during the daily morning meetings. Other traders hated this job. But he developed a liking for commentating and putting forward his views on currencies, in the process helping others. Which he still does today. Moran wrote briefly for Invast Global before taking the position as senior analyst for Royal Financial Trading. He currently is a Responsible Manager in Compliance for Transferwise Ltd, Pty, a global money transfer firm where he advises the Treasury team. Having spent the last 10 years of his trading career managing the Emerging Markets and Asian currency desks of NAB and CBA, he formulates much of his market analysis from their movements. His favourite description for global markets today comes a 1968 hit tune from the group Blood, Sweat and Tears – “What goes up, must come down, spinning wheel got to go round.”