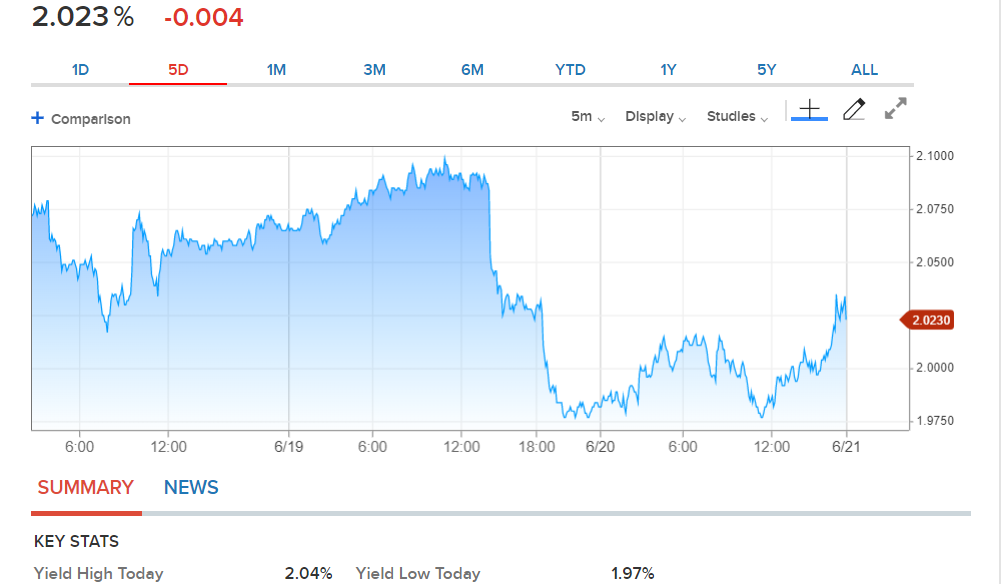

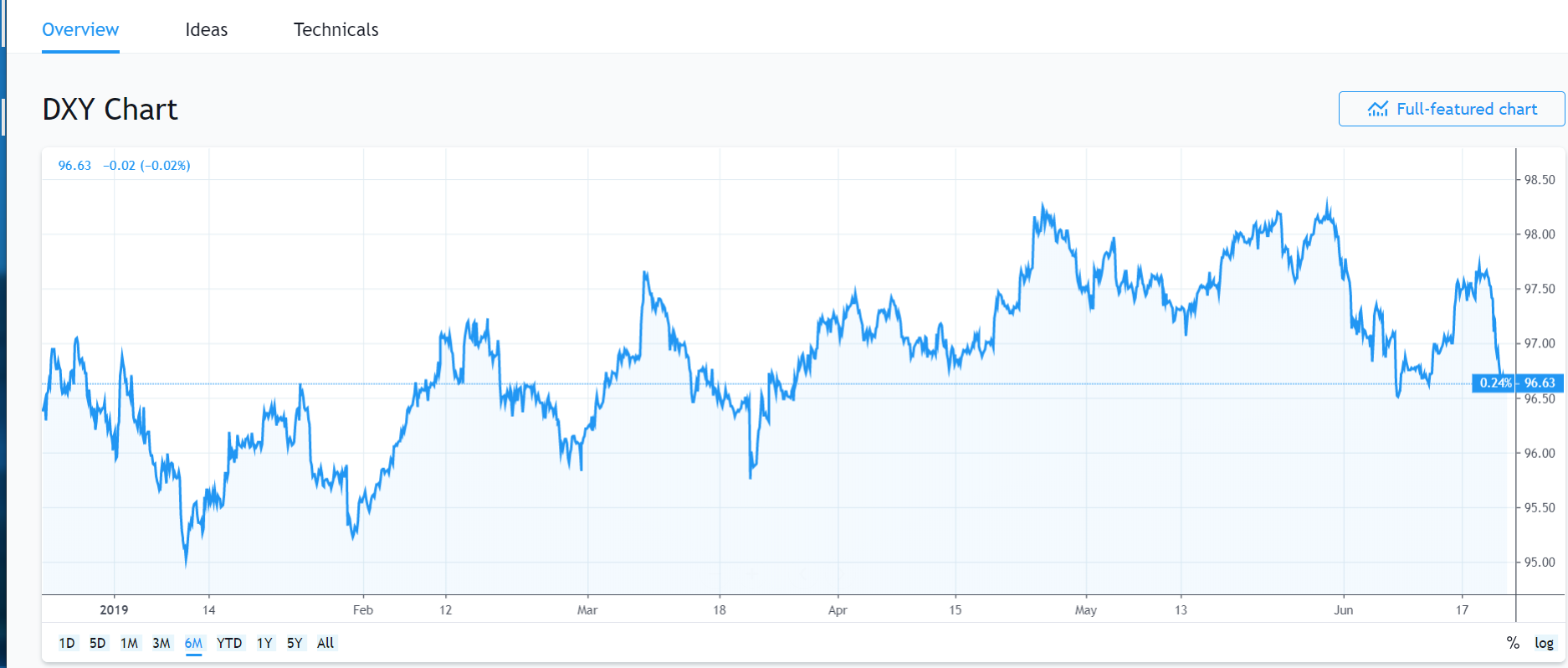

Summary: The Dollar Index (USD/DXY) a popular gauge of the Greenback’s value against 5 major currencies, rebounded off lows to 96.66 after sliding 0.47% to 96.56, its biggest 2-day drop in a year. A dovish turn by the US Federal Reserve, joining the ECB and RBA saw speculators head for the exit and dump their stale Dollar longs. The benchmark US 10-year bond yield steadied to 2.03% after sliding to 1.98%, its lowest level in 2.1/2 years. The Swiss Franc (+1.18% to 0.9817) and Yen (+0.77% to 107.32) outperformed after the Fed signalled it was lower interest rates as early as next month. Sterling rallied 0.31% to 1.2705 lifted by the broad-based US Dollar drop. The Bank of England left interest rates unchanged but was more cautious about global growth. The Euro settled at 1.1294 from 1.1224, off 1-week highs. The Australian Dollar jumped to 0.6925 (0.6885) up 0.5%, lifted by the weakening Greenback and speculative short covering. EM currencies lifted against the Greenback. The offshore Chinese Yuan climbed 0.7% (USD/CNH 6.8600 from 6.8950).

Wall Street stocks climbed. The Dow ended up 0.88% at 26,751 while the S&P 500 was 0.9% up after hitting record highs. Shanghai equities closed 2.38% higher in Asia.

US Philadelphia Fed Manufacturing Index underwhelmed, sliding to 0.3 against a forecast of 10.6.

- USD/DXY – The Dollar Index slid to near 8-day lows at 96.56, settling at 96.66 at the New York close. The overall weaker Greenback pushed USD/DXY lower after hitting 97.76, 3-week highs just a few days ago.

- EUR/USD – the Single currency rallied to finish up 0.5% at 1.1294 (1.1228 yesterday). The Euro fell to 1.1181 on Wednesday after ECB President Mario Draghi hinted at more stimulus in Sintra, Portugal at their global central bank summit.

- AUD/USD – the Aussie Battler rallied on widespread US Dollar weakness and speculative short-covering to 0.6925 at the NY close, up 0.5%.

- USD/JPY – The Dollar slid to 107.33, its lowest level since the flash crash this year. USD/JPY opened at 108.10 yesterday, sliding after 10-year US yields plummeted to 1.98% overnight.

On the Lookout: The Dollar’s overall direction has now shifted south. However, the market once again may have gotten ahead of itself. Expectations have risen for a Fed rate cut with money markets pricing in as many as 3 before the end of the year. This remains to be seen. Economic data releases in the days ahead will be closely monitored.

The US 10-year bond yield finished at 2.03%, one basis point higher from yesterday. In contrast, global rival yields were lower overall by an average of 3 basis points, playing catch-up with those of the US. We can expect some consolidation in the short term before the next big move.

Today sees Australia, Japan, Euro-area (France and Germany), Eurozone, and US Flash Manufacturing and Services PMI data. Japanese National Core CPI, UK Public Sector Borrowing,

Canadian Core Retail Sales and US Existing Home Sales round up today’s economic reports. Markets will be closely monitoring the Manufacturing PMI’s.

Trading Perspective: Expect some consolidation today for the US Dollar. However, long US Dollar market positioning (short currencies) still have a way to go to correct. Reports of a meeting at the G20 summit between Presidents Trump and XI have eased trade tensions and lifted risk appetite.

A good time for flexibility and trading ranges in the short term.

- EUR/USD – The Euro retreated off its highs at 1.13174 to settle at 1.1294, just under its pivot level at 1.1300. Today sees Euro area and Eurozone manufacturing and services PMI data. EUR/USD has immediate resistance at 1.1300 followed by 1.1330. Immediate support can be found at 1.1275 and 1.1250. Ten-year German Bund yields fell 3 basis points to -0.32%, compared to the 1 basis point rally in its US counterpart. This should limit the topside of the Euro for now. Look to trade a likely range today of 1.1275-1.1325. Prefer to buy dips. The speculators are still long of Euro bets.

- AUD/USD – the overall weaker Greenback, higher commodities, stronger Asian currencies and improved risk sentiment all helped boost the Aussie Battler 0.5% to 0.6925. AUD/USD traded to an overnight and 8-day high at 0.69358. The Aussie has immediate resistance at 0.6940 followed by 0.6970. Immediate support can be found at 0.6900 and 0.6870. Look to trade a likely range today of 0.6900-40. We reported earlier in the week that speculative Aussie short bets were at -AUD 63,200 which are near multi-year highs. Prefer to buy dips.

- USD/JPY – The Dollar slid past the 107.80-108.00 support level, slumping to 107.21 yearly lows before settling at its current 107.34 level. The fall in the US bond yield to 1.98%, 2.1/2- year lows triggered short-covering forcing speculative bets to run and cover. The subsequent bounce in the 10-year to 2.03% should see Japanese corporates enter and provide buying support for the Greenback. USD/JPY has immediate support at 107.00 followed by 106.50 which is strong. Immediate resistance lies at 107.70/80 which should hold if gaps are filled. The Bank of Japan left its policy unchanged with no immediate plans to add accommodation. Japanese 10-year JGB yields dropped 4 basis points to -0.18%. Look for a likely trading range today of 107.20-107.70. Look to trade the range shag.

- USD/DXY – The Dollar Index slid to an overnight and 8 day low at 96.567 before settling at 96.66. Immediate support can be found at 96.50 followed by 96.20. Immediate resistance lies at 96.80 and 97.10. Look to trade a likely range today of 96.50-96.80. Prefer to sell rallies. The general direction remains south with the next target 96.00.

Happy Friday and trading all.