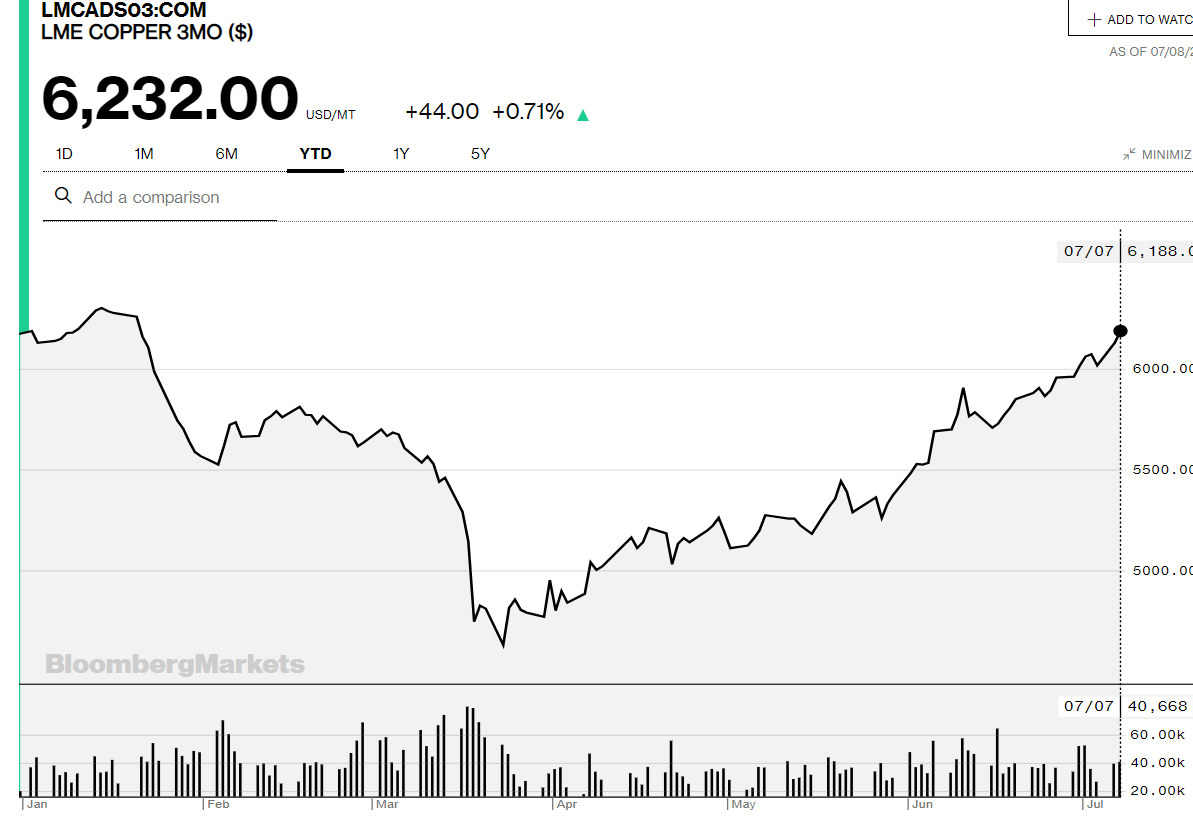

Summary: The Dollar stumbled, hitting 2-week lows as Gold jumped to highs not seen since 2011 (USD 1,818.). The yellow metal continued its grind higher as interest rates remain low in the current monetary expansion. Base metals rallied with Copper prices hitting highs not seen since January. In quiet trade, FX ignored a US daily record of over 60,000 new Covid-19 cases bringing the total to over 3.1 million. Sterling climbed to overnight and 3-week highs at 1.2623 before easing to 1.2615 in late New York from 1.2542 Wednesday. UK Chancellor of the Exchequer Rishi Sunak pledge GBP 30 billion to head off rising unemployment by paying companies to re-hire workers and cut taxes for hospitality firms and homebuyers. The Euro rallied 0.49% to 1.1334 (1.1275 yesterday) at the New York close trading to its 3-week high at 1.13518. Against the Canadian Loonie, which finished as best-forming currency, the Greenback tumbled to 1.3510 (1.3602). Canada’s 10-year bond yield jumped 6 basis points to 0.57% as the central government in Ottawa forecast its largest budget deficit since the Second World War. The Australian Dollar rebounded to 0.6985 (0.6945), despite the resurgence of Covid-19 cases in Victoria and the lockdown in Melbourne. Australia’s post pandemic recovery compared to that of the US and other global hotspots remains healthy. The rise in Base metal prices also supported the Battler. The Greenback also reversed lower against most Emerging Market currencies. The USD/ZAR pair (Dollar-South African Rand) plunged 1.4% to 16.9300 (17.1555) on overall US Dollar weakness and the higher Gold and Commodity prices. USD/CNH (Dollar-Offshore Chinese Yuan) slid just under the 7.00 mark to 6.9990 from 7.0255 yesterday. China’s stock market rose 1.74%. The DOW finished up 0.79% to 26,115 (25,900) while the S&P 500 gained 0.92% to 3,175 (3,147).

Economic Data released yesterday saw Japan’s Current Account Surplus climb to +JPY 0.82 trillion, beating forecasts at +JPY 0.71 trillion. Japan’s Economic Watcher’s Sentiment rose to 38.8 from 15.5, bettering expectations at 24.7. Switzerland’s June Unemployment Rate improved to 3.3% from the previous month’s 3.4%, beating forecasts at 3.6%. US Consumer Credit in June fell to -USD 18.3 billion, missing expectations of -USD 15.2 billion.

On the Lookout: Expect a slow start in Asia with the risk-on theme from last night to carry forward. FX and risk markets ignored the ongoing resurgence in Covid-19 new cases beginning in the US and following other current hotspots in the world. The optimism comes from anticipated further fiscal measures and growing expectations of a successful vaccine. Yesterday US virus expert Doctor Anthony Fauci said Phase 3 vaccine trials may begin at end-July and that he is “cautiously optimistic” for a vaccine by year-end.

Data released today are light. Japan kicks off in Asia with its Core Machinery Orders and Preliminary Tools Orders data. New Zealand releases its ANZ Business Confidence Survey. Australia releases its Home Loans data for May. China follows with its CPI and PPI (y/y) reports. Europe sees Germany’s Trade Balance and Current Account reports while the Euro group meetings kick off today. Canada kicks off North American reports with its June Housing Starts. The US finish off the day’s reports with its Weekly Unemployment Claims.

Trading Perspective: The Dollar failed to extend gains and reversed lower. The Dollar Index (USD/DXY) a favourite gauge of the Greenback’s value against a basket of 6 major currencies slumped 0.42% to 3-week lows at 96.476 (96.980). While we can expect some early Asian pressure on the US Dollar, there will need to be fresh impetus to drive the Greenback lower. Otherwise, as we head into the Northern Hemisphere summer season, which traditionally sees a lull in FX, consolidation will be the order of the day. The uncertainty for this latest resurgence in Covid-19 cases led by the US and other global hotspots remains. With rising new cases comes the real risk of rising new deaths despite the slowing of death rates recently. We look at a few currencies.

AUD/USD – Firm Commodities Drive Battler Up, Virus Rise Caps at 0.7030

The Australian Dollar held above 0.69 cents, trading to an overnight low at 0.69274 in mild overnight trade. The negative sentiment at the start of trade yesterday due to the alarming rise of new cases in Victoria which resulted in Melbourne’s city-wide lockdown kept the Aussie under pressure. The steady rise of Gold prices, which was already occurring in the background saw the yellow metal rally above the USD1,800 mark, lifting other commodities, including base metals. Copper prices rose 0.71% to hit highs not seen since late January this year. Traders also chose to focus on Australia’s post coronavirus recovery which, compared to that of the US, remains healthy. While that is the case, the cost of this second wave of Covid-19 cases could upset Australia’s economic recovery.

AUD/USD has immediate resistance at 0.7000 cents followed by 0.7030. Immediate support can be found at 0.6960 with 0.6920 as the next support, which is strong. We reported yesterday that the latest Commitment of Traders report saw net speculative AUD short bets to their smallest in two years. The market is no longer short. Look for consolidation today in a likely range of 0.6920-0.7020. Prefer to sell rallies.

EUR/USD – Climbs on Broad-Based USD Weakness, 1.1380 Caps

The Euro advanced 0.49% against the US Dollar, finishing at 1.1332 in New York. Broad-based Greenback weakness enabled the shared currency to rally. While an upbeat UK budget supported the British Pound, still no Brexit deal was forthcoming. Yesterday saw some optimism on Brexit which saw the promise of a compromise deal on a food supply issue. Germany’s Angela Merkel said that we should prepare for the possibility of not reaching a Brexit deal with the UK.

We reported yesterday that net Euro long bets in the latest COT report (week ended June 30) were slashed by -EUR 19,493 contracts to a net long of +EUR 98,955 contracts. Total net speculative long Euro bets were still at 84% relative to the year’s maximum number of longs.

EUR/USD has immediate resistance at 1.1350 followed by 1.1380. Immediate support can be found at 1.1310 followed by 1.1270. Look for consolidation within a likely range today of 1.1270-1.1370. Prefer to sell rallies to 1.1370.

USD/CAD – Loonie Outperforms on Yield Spike, Debt Shortfall Will Weigh

The Canadian Loonie jumped against its US counterpart supported by stronger Gold and commodities prices and higher bond yields. USD/CAD tumbled to an overnight low at 1.34928 before rallying in late New York to 1.3510. Reuters reported that Canada’s long-term debt rose by the most in nearly four months as Ottawa forecast its largest budget shortfall since the Second World War. The yield on Canada’s 10-year bond climbed 6 basis points to 0.57% from 0.51% yesterday. In contrast the key US 10-year treasury rate was up 2 basis points to 0.66%.

In the longer run a budget deficit will result in a weaker currency, not stronger. Much of the Loonie’s gains were also fuelled by the market’s risk-on stance as equities rallied. The latest Commitment of Traders report (week ended June 30) saw net speculative CAD shorts trimmed modestly to -CAD 20,519 contracts from the previous week’s -CAD 20,834.

USD/CAD has immediate support at 1.3490 followed by 1.3450. Immediate resistance can be found at 1.3530 followed by 1.3580 and 1.3620. Look for consolidation in a likely range between 1.3490-1.3590. Prefer to buy USD/CAD dips.