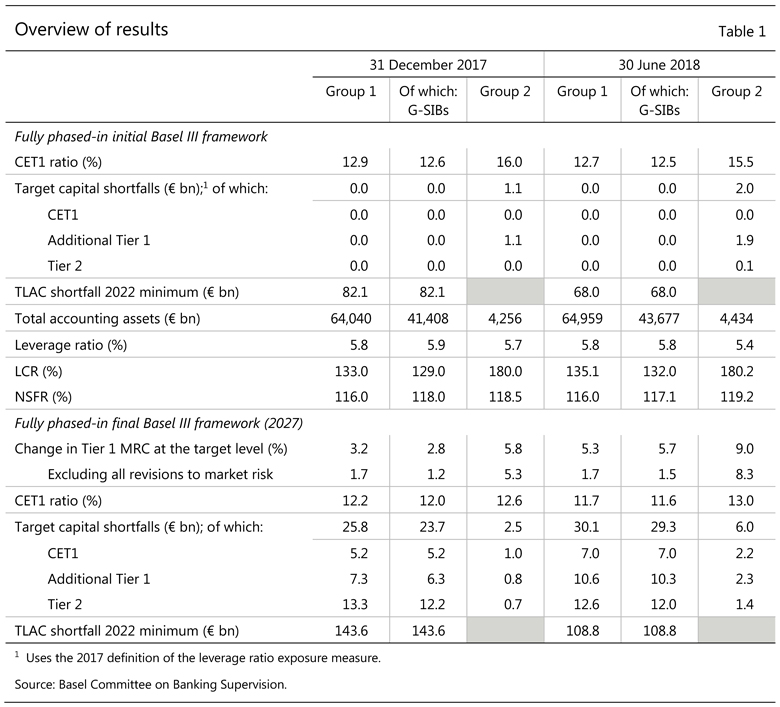

- Changes in minimum required capital from fully phased-in final Basel III remain stable for large internationally active banks compared with end-2017

- All banks continue to meet initial Basel III minimum and target CET1 capital requirements

- All banks in the sample reported Liquidity Coverage Ratios (LCRs) that met or exceeded the final 100% minimum requirement

The Basel Committee today published the results of its latest Basel III monitoring exercise, based on data as of 30 June 2018. Through a rigorous reporting process, the Committee regularly reviews the implications of the Basel III standards for banks, and has been publishing the results of such exercises since 2012. The report sets out the impact of the Basel III framework that was initially agreed in 2010 as well as the effects of the Committee’s December 2017 finalisation of the Basel III reforms. However, it does not yet reflect the finalisation of the market risk frameworkpublished in January 2019.

Data are provided for a total of 189 banks, including 106 large internationally active banks. These “Group 1” banks are defined as internationally active banks that have Tier 1 capital of more than €3 billion, and include all 29 institutions that have been designated as global systemically important banks (G-SIBs). The Basel Committee’s sample also includes 83 “Group 2” banks (ie banks that have Tier 1 capital of less than €3 billion or are not internationally active).

The final Basel III minimum requirements are expected to be implemented by

1 January 2022 and fully phased in by 1 January 2027. On a fully phased-in basis, the capital shortfalls at the end-June 2018 reporting date are €30.1 billion for Group 1 banks at the target level. These shortfalls are more than 70% smaller than in the end-2015 cumulative QIS exercise, thanks mainly to higher levels of eligible capital. For Group 1 banks, the Tier 1 minimum required capital (MRC) would increase by 5.3% following full phasing-in of the final Basel III standards relative to the initial Basel III standards. This compares with an increase of 3.2% at end-2017.

The increases in both shortfalls and the change in MRC over the last six months are driven partly by a higher market risk contribution; this does not yet reflect the finalisation of the market risk framework published in January 2019, which is expected to offset the increases to some extent. By excluding all revisions to the market risk framework, the current end-June 2018 data show increases in Tier 1 MRC of 1.7%, 1.5% and 8.3% for Group 1 banks, G-SIBs and Group 2 banks, respectively, compared to 1.7%, 1.2% and 5.3% six months earlier.

The initial Basel III minimum capital requirements were fully phased in by 1 January 2019 (while certain capital instruments can still be recognised for regulatory capital purposes until end-2021). On a fully phased-in basis, data as of 30 June 2018 show that all banks in the sample continue to meet both the Basel III risk-based capital minimum Common Equity Tier 1 (CET1) requirement of 4.5% and the target level CET1 requirement of 7.0% (plus any surcharges for

G-SIBs, as applicable). In addition, applying the 2022 minimum requirements for total loss-absorbing capacity (TLAC), six out of 24 G-SIBs reporting TLAC data have a combined incremental TLAC shortfall of €68 billion as at the end of June 2018, compared with €82 billion at the end of December 2017.

The monitoring reports also collect bank data on Basel III’s liquidity requirements. Basel III’s Liquidity Coverage Ratio (LCR) was set at 60% in 2015, increased to 90% in 2018 and continued to rise in equal annual steps to reach 100% in 2019. The weighted average LCR for the Group 1 bank sample was 135% on

30 June 2018, compared with 133% six months earlier. For Group 2 banks, the weighted average LCR remained almost stable at 180%. All banks in the sample reported an LCR that met or exceeded the final 100% minimum requirement.

Basel III also includes a longer-term structural liquidity standard: the Net Stable Funding Ratio (NSFR). The weighted average NSFR for the Group 1 bank sample remained stable at 116%, while for Group 2 banks the average NSFR increased slightly to 119%. As of June 2018, 96% of the Group 1 banks and 95% of the Group 2 banks in the NSFR sample reported a ratio that met or exceeded 100%, while all banks reported an NSFR at or above 90%.