Resolution is the process by which authorities intervene to manage the failure of a bank in an orderly way. This process reduces risks to depositors, the financial system, and public finances. The financial crisis, in which governments used taxpayer money to bail out banks and their losses, showed the need for an effective resolution regime as disorderly bank failure is disruptive and costly.

The Resolvability Assessment Framework (the framework) establishes the capabilities firms should have and the outcomes they must achieve to be resolvable. The framework is designed to make sure firms are accountable for their own resolvability. This is done by setting out a clear framework as to how the Bank will assess firms’ resolvability and requiring major UK firms publicly disclose a summary of their own resolvability assessment. The framework is implemented by:

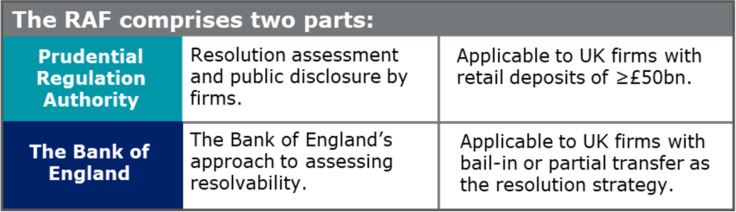

- The Bank of England’s approach to assessing resolvability, as set out in the Statement of Policy published today. The Bank will assess firms against three resolvability outcomes they must meet by 2022: i) having adequate financial resources, ii) being able to continue to do business through resolution and restructuring, and iii) being able to communicate and coordinate within the firm and with authorities. This applies to all UK firms with a bail-in or partial transfer resolution strategy and material UK subsidiaries of overseas-based firms.

- The PRA’s new requirements on firms as set out in the new Resolution Assessment part of the PRA Rulebook and the accompanying Supervisory Statement. The PRA rules require major UK banks, with £50bn or more in retail deposits, to assess their preparations for resolution, submit reports of their assessment to the PRA and publicly disclose a summary of their report. As per the consultation paper, these assessments and disclosures will work on a two-year cycle. Firms will submit the first of these reports on their resolution assessments to the PRA by October 2020 and publicly disclose their summaries by June 2021.

As part of the new framework, the Bank will publicly disclose this assessment for the major UK banks for the first time. The intention is for this to take place at the same time as the firms make their own disclosures.

The framework is an important step towards delivering the Bank’s commitment to Parliament that major UK banks will be resolvable by 2022. Accountability and transparency of firms’ resolvability will increase public awareness of resolution, help market participants make better informed investment decisions and incentivise firms to meet the resolvability outcomes by 2022.

The framework and the resolution regime will allow bank services to continue during and after resolution, so that authorities or new management can restructure the bank as necessary. This reduces the risks to depositors, the financial system and taxpayers.

Deputy Governor for Financial Stability, Jon Cunliffe, said: “We have made major reforms since the financial crisis to make firms resolvable and ensure that those who profit from banks’ success also pay when they fail. Increased transparency about the resolution regime is in the public’s interest and also incentivises firms to make further progress on their resolvability.”

Deputy Governor for Prudential Regulation and Chief Executive Officer of the Prudential Regulation Authority, Sam Woods, said: “The framework we have published today will build on the significant reforms made to the resolution regime over the past few years and contribute to a safer financial system.”