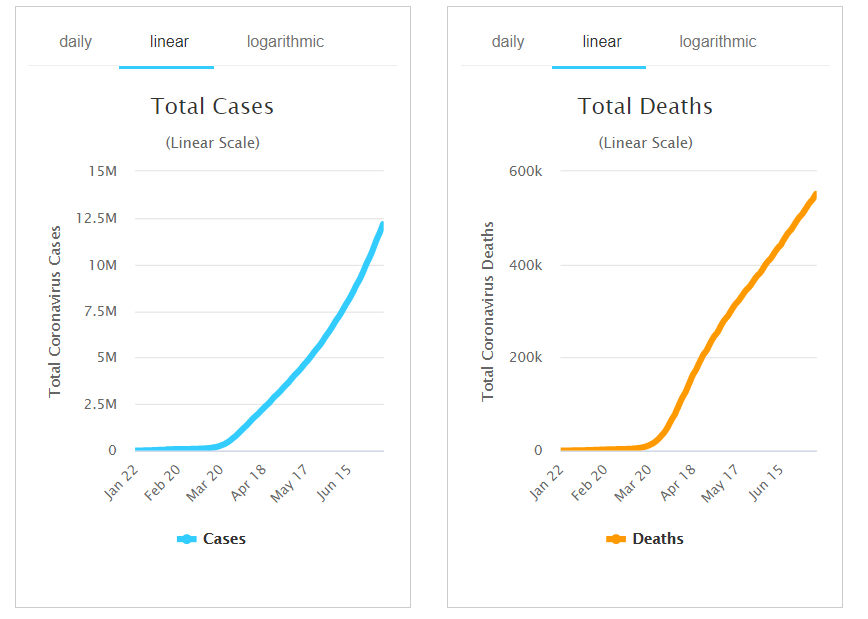

Summary: Risk wars extended with a surge in new global Covid-19 infections foiling a record rise in the tech-heavy US NASDAQ. In the US, the daily number of new coronavirus cases topped 60,000, a fresh one-day record. The resurgence of Covid-19 infections continued in other parts of the world. In cities such as Tokyo and Melbourne, restrictive measures returned as a rise in daily virus were also recorded. Also aiding the Greenback’s rise was a US Supreme Court ruling that President Trump cannot block the release of his financial records to prosecutors. The Dollar Index (USD/DXY), a favoured gauge of the US currency’s value against a basket of 6 major currencies, rebounded 0.33% off 4-week lows to 96.792 (96.476). The Euro retreated from a one-month high to 1.1282 (1.1334 yesterday) as the stronger Greenback and overbought conditions weighed on the shared currency. Sterling edged lower to finish at 1.2605 after peaking at 1.2670 overnight. Risk currencies slid. The Australian Dollar slipped 0.39% to 0.6962 after failing to clear 0.70 cents. Against the Canadian Loonie, the Greenback soared to 1.3585 from 1.3512 as Oil prices slumped. The Dollar dropped to 4-month lows against the Offshore Chinese Yuan (USD/CNH) to 6.9960 (7.0010 yesterday) as China’s benchmark Shanghai Stock Exchange saw a 9% rally so far this week on optimism over new policies would liberalise the country’s financial markets. Wall Street stocks closed mixed. The NASDAQ closed higher at 10,745 (10,685) while the DOW ended down 1.57% to 25,705 (26,115). The S&P 500 lost 0.74% to 3,152 (3,175). Global bond yields dropped. The benchmark US 10-year treasury yield fell 5 basis points to 0.61%. Germany’s 10-year Bund yield was at -0.46% (-0.44% yesterday).

Data released yesterday saw Japanese Core Machinery Orders rose 1.7%, beating forecasts for a drop at -5.2% and a previous -12.0%. Germany’s May Trade Surplus climb to +EUR 7.6 billion from the previous month’s +EUR 3.2 billion. Canada’s Housing Starts climbed to 212,000 units beating expectations of a 185,000 rise. US Claims for Unemployment Benefits dip to 1.314 billion, bettering forecasts of 1.375 billion.

On the Lookout: The election uncertainty is now becoming a factor for the markets which should provide support from safe-haven flows into the Dollar. Trade tensions appear to be on the ascent again. Markets will be monitoring any new developments on this front.

Today’s data calendar is relatively light. Japan kicks off with its annual PPI report for June. Earlier in the day New Zealand’s Electronic Card Retail Sales rose 16.3%, which did not budge the Kiwi. China reports its June New Loans data. Europe enters the market with France’s Industrial Production followed by Italian Industrial Production data for May. Canada releases its June Payrolls report, Unemployment Rate, and Average Hourly Wages. The US rounds up the day’s data with its Headline and Core Producer Price Index (PPI) for June.

Trading Perspective: Markets will continue to monitor the rising spread of the coronavirus around the world. Which could see more restrictions returned for economies and weigh on risk sentiment. The daily total of new deaths has also risen, led by the US with 710 and Brazil with 1,129 as at yesterday. If these of numbers (new daily cases and new daily deaths) grow, it will see risk-off big-time. Traders will also look out for the next stage of fiscal measures to battle the virus outbreak. The US is expected to announce its fiscal stimulus between July 20-31 according to Treasury Secretary Steven Mnuchin. We look at a few currencies.

AUD/USD – Upside Momentum Wanes, Further Covid-19 Spike Forecast in Victoria

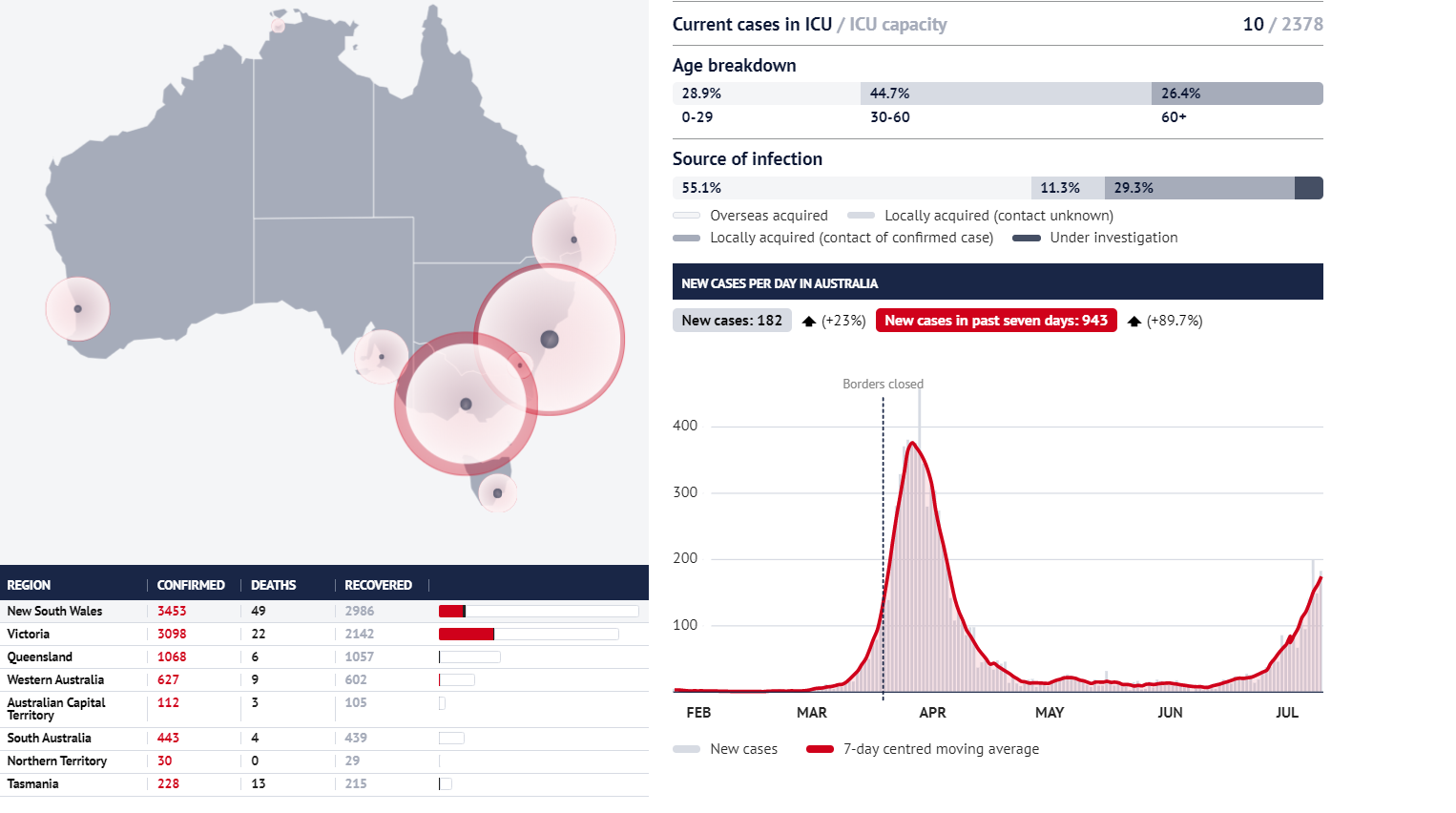

The Australian Dollar’s upside momentum waned after its failure to clear above 0.7000 cents yesterday even as Victoria recorded 165 new coronavirus cases yesterday, its second highest daily total. In the neighbouring state of New South Wales (Australia’s largest state by population), Premier Gladys Berejiklian warned that it would be several weeks before NSW knows where Covid-19 has made a resurgence despite closing the border with Victoria according to the Sydney Morning Herald in a report today. Further spikes in Victoria are forecast.

The overall stronger Greenback also weighed on the Aussie Battler. AUD/USD closed in New York at 0.6963 after trading to an overnight low at 0.69502. The Aussie peaked at 0.7001 earlier in the Asian session as China’s Offshore Yuan and other Asian currencies rallied. AUD/USD has immediate resistance at 0.6980 and 0.7010. Immediate support can be found at 0.6950 followed by 0.6920 and 0.6880. Look for the AUD/USD to grind lower in a consolidation today which is likely between 0.6910-0.6980.

EUR/USD – Retreating as Safe Haven Support from Covid-19 Fear Lifts US Dollar

The Euro retreated below 1.1300 to 1.1282 NY close after recording an overnight and 4-week high at 1.13708. The broad-based US Dollar rebound and a largely overbought speculative market weighed on the shared currency. Also weighing on the currency is evidence from recent economic data of Germany’s external demand and industrial production lagging behind domestic consumption. ING Bank’s Chief Economist Carsten Brzeski observes that July data will be key for the future path of monetary policy. The ECB’s policy meeting and rate announcement falls next week.

The latest Commitment of Traders/CFTC report saw net speculative EUR long bets cut to +EUR 98,955 in the week ended June 30. Net total speculative long Eur bets are still at multi-year highs. While net long bets have been trimmed, there has yet to be a decent correction.

EUR/USD has immediate support at 1.1280 (overnight low) followed by 1.1250. Immediate resistance can be found at 1.1310 and 1.1340. Look for a gradual drift lower in the Euro with a likely range between 1.1240-1.1320. Prefer to sell rallies.

Michael Moran

Michael Moran is an experienced global markets professional who currently writes a daily markets commentary. Moran has traded currencies for over 30 years, having worked in dealing rooms of major banks all over the globe. He lives in Sydney with his wife, 5 children, 2 grandsons and another coming. He still loves trading and talking about the currency markets. All of them! Michael began his career as an assistant dealer in money markets and foreign exchange with Lloyds Bank. He has worked in Hongkong, Manila, Tokyo, Singapore and Sydney. He’s traded through the 1985 Plaza Accord, Paul Keating’s 1986 “banana republic” statement, the Asian Currency Crisis in 1997, and the 9/11 New York Twin Tower terrorist strike. He took the task of speaking to sales team of the banks he worked at (Lloyds, NAB, CBA) during the daily morning meetings. Other traders hated this job. But he developed a liking for commentating and putting forward his views on currencies, in the process helping others. Which he still does today. Moran wrote briefly for Invast Global before taking the position as senior analyst for Royal Financial Trading. He currently is a Responsible Manager in Compliance for Transferwise Ltd, Pty, a global money transfer firm where he advises the Treasury team. Having spent the last 10 years of his trading career managing the Emerging Markets and Asian currency desks of NAB and CBA, he formulates much of his market analysis from their movements. His favourite description for global markets today comes a 1968 hit tune from the group Blood, Sweat and Tears – “What goes up, must come down, spinning wheel got to go round.”