Around 26 million Brits use an overdraft each year. Overdrafts are either arranged or unarranged. An arranged overdraft is an agreement consumers reach with their bank that allows them to spend more than they have in their account up to a specific limit. The limit and interest fees are agreed upon in advance. An unarranged overdraft is an overdraft consumers have not agreed on with their bank. An account enters an unarranged overdraft when it is overdrawn or the amount overdrawn goes above your arranged overdraft limit.

The FCA announced the following changes as of this year:

1. Banks must introduce a single annual interest rate or EAR on all overdrafts

2. Charges for unarranged overdrafts can no longer be higher than for an arranged overdrafts

3. Banks must eliminate any fixed fees (i.e. daily or monthly fees)

4. The advertising and pricing of overdrafts must be standardised so the customer can compare overdraft offers

5. Refused payment fees need to correspond to the amount of the refused payment

6. Banks must do more to identify customers in financial difficulty and help them reduce their use of overdrafts

As a result of these changes, many banks have increased their annual interest rates on overdrafts. Barclays has one of the lowest interest rates of the high-street banks charging 35% EAR. Natwest now charge an EAR of 39.49%, Santander and HSBC have upped their EAR to 39.9%, and Lloyds have changed their interest rates to between 27.5% and 49.9% EAR.

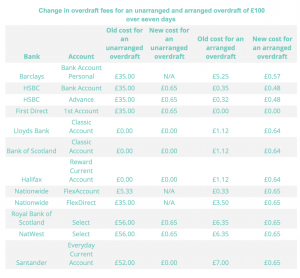

Although the new interest rates may seem high, this is good news for consumers with unarranged overdrafts. The costs for unarranged overdrafts have decreased significantly, as the table below shows. However, some banks such as Barclays and Nationwide are no longer offering unarranged overdrafts to their customers. For Lloyds, Bank of Scotland and Halifax customers, there are no changes in charges for borrowing £100 over 7 days. Arranged overdraft customers, on the other hand, may find themselves worse off after the changes. The cost of the average arranged overdraft at HSBC, for example, has risen to £6.96 to £11.76 annually.

Data for Portify’s guide to overdrafts in 2020 shows banks have not only changed the way they charge fees for overdrafts, but have also have reduced or eliminated any interest-free buffer’s on overdraft facilities. TSB previously offered at least a £35 interest-free buffer on all accounts. The bank has now removed the interest-free buffer on unarranged overdrafts completely, as have Lloyds.”