Summary: A warning by Dr. Anthony Fauci, director of the US National Institute of Allergy and Infectious Diseases that a premature opening of the economy could lead to Covid-19 outbreaks saw Wall Street stocks slump while the Dollar was mostly lower. The CBOE Volatility Index (VIX), also known as the fear index or gauge, jumped 19.8% to 33.04, its largest one-day rise in over three weeks. Reports of new coronavirus clusters in China, South Korea, and Germany where lockdowns have been lifted added to investor’s anxiety. In FX, the Dollar was mostly lower after US treasuries rose and bond yields eased. The Euro rebounded to 1.0848 after hitting an overnight low of 1.07843, up 0.34% against the Dollar. Sterling though, came under selling pressure, falling to 1.2260 (1.2335) as UK Prime Minister Boris Johnson and his government try to bring Britain out of their lockdown. The US Dollar fell back against the Yen to 107.15 from 107.65 as the key US 10-year bond yield dropped to 0.67% from 0.71%. Risk currencies retreated. The Australian Dollar lost 0.26% to 0.6470 (0.6490) while the Kiwi (New Zealand Dollar) dipped 0.2% to 0.6075 (0.6088) ahead of today’s RBNZ policy meeting and rate announcement. Against the Canadian Loonie, the Dollar rose 0.4% to 1.4075 (1.4015). The Dollar Index (USD/DXY), a favoured gauge of the Greenback’s value against a basket of major currencies, slipped 0.23% to 100.04 (100.19). Fedspeak saw a dire outlook from several regional heads. Bloomberg reported that Governor and FOMC member Randal Quarles warned that “the Fed could curtail Wall Street banks’ ability to pay dividends by cranking up the amount of capital needed to maintain due to the coronavirus crisis.” Dallas Fed President Robert Kaplan said the economy will need more fiscal stimulus if the unemployment rate continues to rise.

The DOW was 2.58% lower to 23,594 (24,215) while the S&P 500 fell 2.77% to 2,847 (2,927).

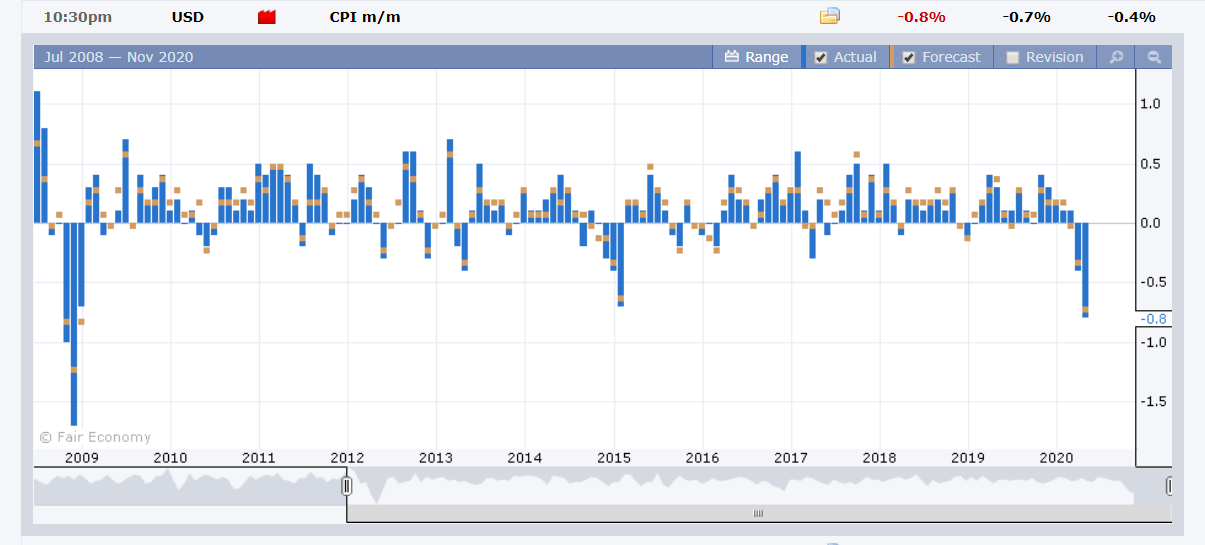

Data released yesterday saw US Headline CPI in April drop to -0.8% from March’s -0.4%, lower than median forecasts at -0.7%. It was the biggest decline since 2008. Core CPI slumped to -0.4% from -0.1%, under most forecasts at -0.2%. China’s Annual CPI in April fell to 3.3% from 4.3%, underwhelming forecasts at 3.7%. Chinese PPI (annual) fell to -3.1% from -1.5%, missing forecasts at -2.6%.

On the Lookout: Events and data releases pick up today beginning with the RBNZ’s Official Cash Rate decision and Statement (12 noon, Sydney time). Which puts the spotlight on the Kiwi (NZD/USD). New Zealand’s Official Cash Rate currently stands at 0.25%, just above zero which would make a cut unlikely. If Governor Graeme Orr and his colleagues do ease, it would most likely come via additional QE. New Zealand has begun to reopen businesses and schools and it may not be necessary for the RBNZ to ease. Instead they may opt to leave the door open to additional easing. Which should steady the Bird (NZD/USD).

The other big event is Fed Chair Jerome Powell’s update on the economy at a webinar (11 pm Sydney time). While markets expect the Fed to provide additional stimulus, the big question is whether they will go to negative rates. US yields have bounced back after Friday’s Payrolls report.

UK Q1 GDP heads today’s data releases. Prior to that, Asia sees Japanese Bank Lending, Current Account and Economic Watchers Sentiment Index; Australia’s Westpac Consumer Sentiment and Q1 Wage Price Index. The UK also releases its monthly Manufacturing Production, April GDP, Construction Output, Industrial Production and Goods Trade Balance. US reports round up the day with Headline and Core PPI.

Trading Perspective: Risk appetite will continue to dominate FX. Current fears of another wave of Covid-19 breakout amidst attempts to reopen economies, China-US/Coalition trade war and dire economic data releases will continue to weigh on sentiment. While the Dollar Index (USD/DXY) was lower, the Greenback put in a mixed performance against its rivals, rising against risk currencies (AUD,NZD,CAD) while lower against the traditional havens (JPY, CHF), including the Euro. Sterling fell ahead of key UK Q1 GDP today. Expect this theme to continue in Asia. Best way to trade these markets is defensive, keeping in mind levels from trading ranges, market positioning and staying flexible. We look at the individual currencies.

NZD/USD – RBNZ Unlikely to Ease, Kiwi Steady; 0.60-0.62 Likely Ahead

The Kiwi/Bird/New Zealand Dollar dipped against the USD to 0.6075 from 0.6088 yesterday ahead of today’s RBNZ interest rate decision. New Zealand’s central bank likely to leave its Official Cash Rate unchanged at 0.25%. Traders are focussed on the RBNZ’s Quantitative Easing program as well as forward guidance on interest rates. Traders will be looking at the RBNZ’s language. Any mention of negative rates from Governor Graeme Orr and his colleagues will weigh on the Kiwi. In April Orr said that negative rates are not ruled out and they will be thinking about additional stimulus.

With New Zealand about to end its lockdown having just opened businesses and schools, the RBNZ will refrain from easing but keep the door open.

In this case, the Kiwi should hold on to its gains. NZD/USD has immediate support at 0.6040 followed by 0.6010. Immediate resistance can be found at 0.6120 followed by 0.6170. The latest COT report saw a modest increase in NZD short bets to -NZD 14,953 contracts from the previous week’s -NZD 13,799., which is 35% of the year’s highs. Which says there are no big positions currently. Look for consolidation in a wider 0.6000-0.6200 range, trade both sides at the extremes is the best strategy.

AUD/USD – Risk-Off, China Trade Ban Depress Battler; RBNZ; Aussie Wages Next

The Aussie Dollar slipped 0.26% to 0.6467 (0.6490) as risk sentiment soured while China yesterday banned meat imports from four Australian processors. While Chinese customs said it found the beef products from certain Aussie firms violated inspection requirements, it was a clear retaliatory move on Prime Minister Scott Morrison’s push for an inquiry into China’s role in the spread of Covid-19.

AUD/USD stayed under the 0.6500 resistance level, slipping to an overnight low at 0.64320 before rallying to 0.6467 at the New York close. Today the spotlight for Aussie traders falls on the RBNZ rate decision and its impact on the Kiwi. The ongoing US-China trade war as well as growing fears of a fresh rise of coronavirus cases in Germany, Korea and China following an easing in lockdown restrictions will weigh on the Aussie Battler. Market positioning though supports the Aussie. Speculative short Aussie bets were trimmed in the latest COT report (week ended May 5) to -AUD 33,455 contracts from -AUD 37,741. While the number is smaller, it is still 50% of the yearly high.

AUD/USD has immediate support at 0.6430 followed by 0.6400 and 0.6370. Immediate resistance can be found at 0.6500 followed by 0.6540 and 0.6580. Look for the Aussie to remain pressurised within a likely 0.6410-0.6510 range today. Look to trade either extreme, we could see some volatility ahead.