Good morning. I am honored and delighted to participate in this second annual conference on global risk, uncertainty, and volatility, cosponsored by the Federal Reserve Board, the Bank for International Settlements, and the Swiss National Bank.1 I would like especially to thank the Swiss National Bank for hosting this event. This conference is part of continuing work across all of our institutions and the academic community to better quantify and assess the implications of risk and uncertainty. I am pleased that this year the focus of the conference is on two of my long-standing professional interests—financial markets and monetary policy. And my remarks today will not stray far from those interests. In particular, I would like to address an issue that has been much in focus—the decline in long-term interest rates—highlighting the role of monetary policy in contributing to that decline and the implications of that decline for the conduct of monetary policy.

The Decline in Long-Term Interest Rates and the Role of Monetary Policy

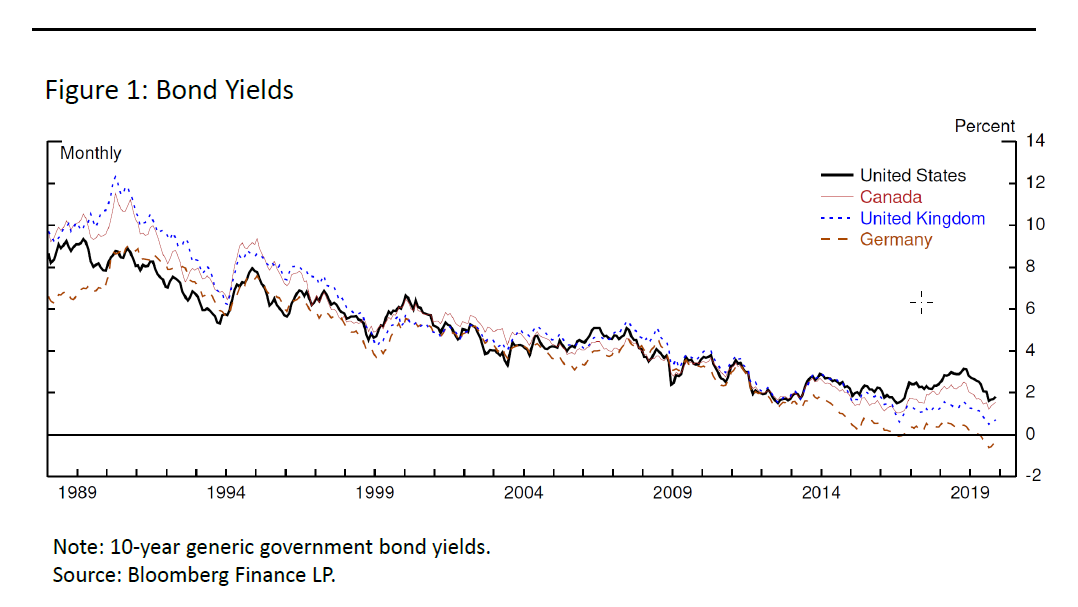

One of the most remarkable and fundamental changes in the global financial landscape over the past three decades has been the steady and significant decline in global sovereign bond yields. From the late 1980s, when 10-year nominal Treasury yields in the United States and sovereign rates in many other major advanced economies were around 10 percent, global bond yields in the advanced economies have trended lower to levels below 2 percent today (figure 1, “Bond Yields”).

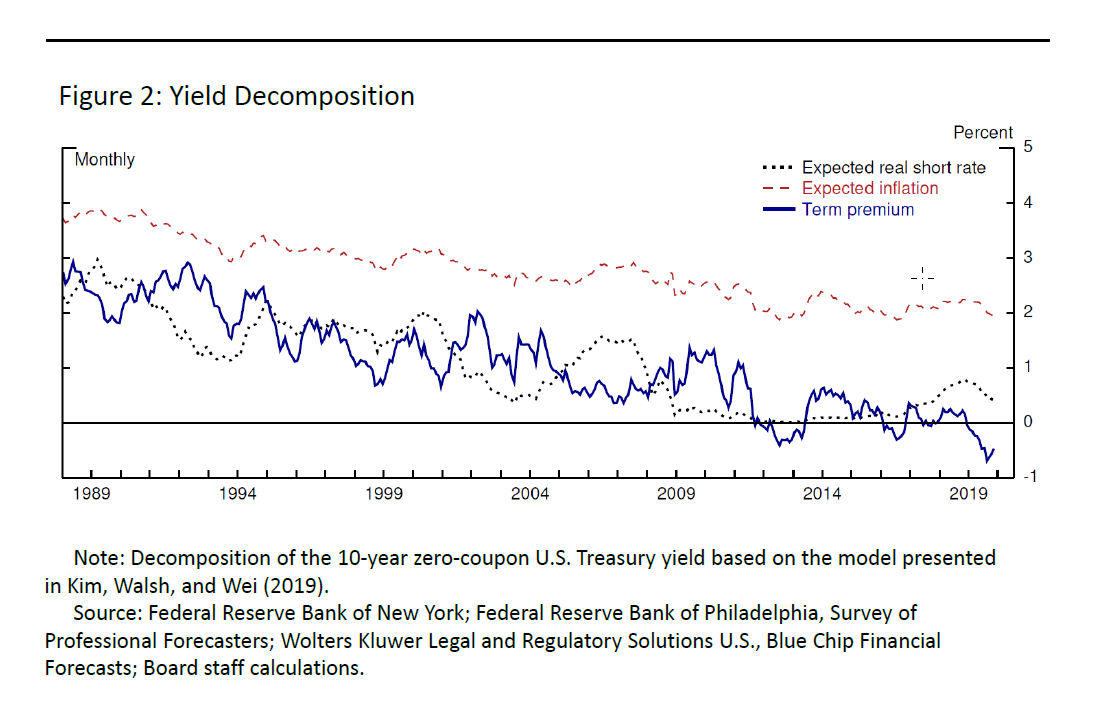

To understand and interpret this decline, it is useful to think of the yield on a nominal 10-year bond as the sum of two components: investors’ expectation over the next 10 years of the average level of short-term interest rates plus a term premium. The term premium is the additional compensation—relative to investing in and rolling over short-maturity bills—that bondholders require for assuming the risk of holding a long-duration asset with greater exposure to interest rate and inflation volatility. Importantly, according to economic theory the equilibrium term premium can be negative. In this case, which is relevant today in the United States and some other countries, the exposure to interest rate and inflation volatility embedded in a long-maturity bond is more than offset by the potential value of the bond in hedging other risks, such as equity risk.2 The expectation of the average level of future short-term interest rates can, in turn, be decomposed into the expectation of average future real interest rates and the expectation of average future inflation rates. Performing this standard decomposition reveals that the decline in long-term rates reflects declines in all three components: expected real rates, expected inflation, and the term premium (figure 2, “Yield Decomposition”). I will now discuss each of these components in turn.

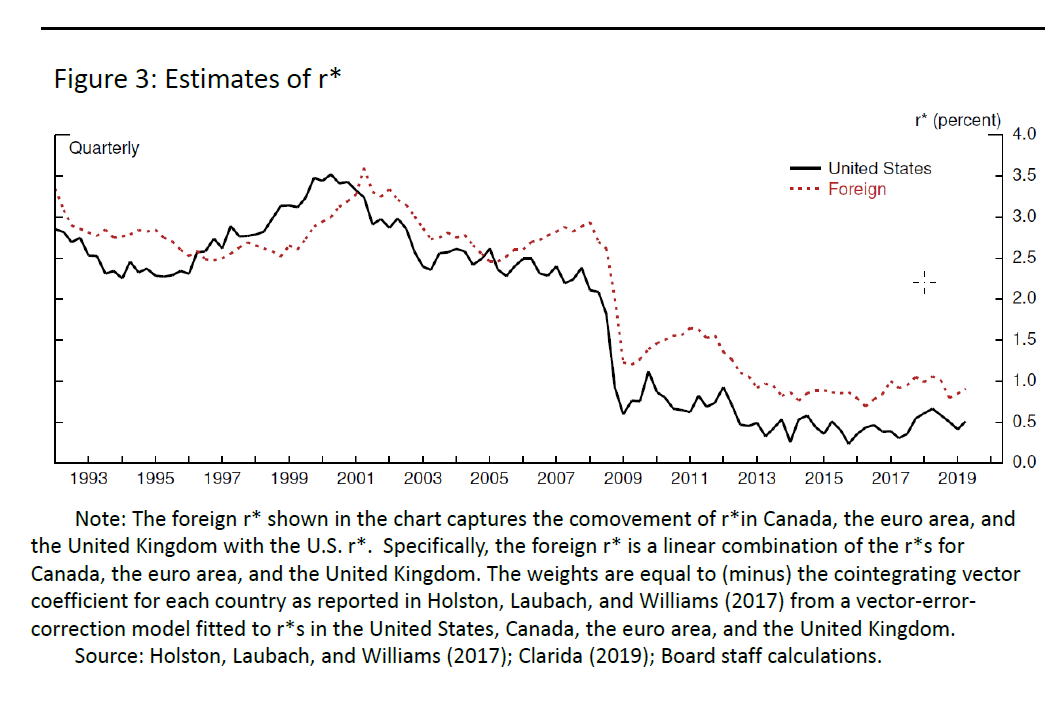

With respect to expected real short-term interest rates, one reason investors expect lower future short-term interest rates is that neutral interest rates appear to have declined worldwide and are expected to remain low. This concept of a neutral level for short-term real interest rates is referred to in the academic literature as r* and corresponds to the rate consistent with a level of aggregate demand equal to and growing in pace with aggregate supply at an unchanged rate of inflation. Longer-run secular trends in r* largely, or even entirely, reflect fundamental “real” factors that are outside the control of a central bank. Policymakers and academics alike, including myself, have spent considerable time exploring the reasons for and ramifications of the decline in r* across countries.3 For example, many have pointed to slowing population growth and a moderation in the pace of technological change as consistent with a lower level of r*.4 Changes in risk tolerance and regulations have led to an increase in savings and in the demand for safe assets, pushing down yields on sovereign bonds.5 Importantly, economic theory suggests and empirical research confirms that there is a significant common global component embedded in individual country r*s (figure 3, “Estimates of r*”).6 This common factor driving individual country r*s not only reflects the influence of common global shocks affecting all economies in a similar way (for example, a slowdown in global productivity and the demographics associated with aging), but also results from international capital flows that respond to and, over time, tend to narrow divergences in rates of return offered across different countries. Other things being equal, a decline in the common factor driving individual country r*s that is evident in the data would be expected to produce a comparable common decline in global bond yields.

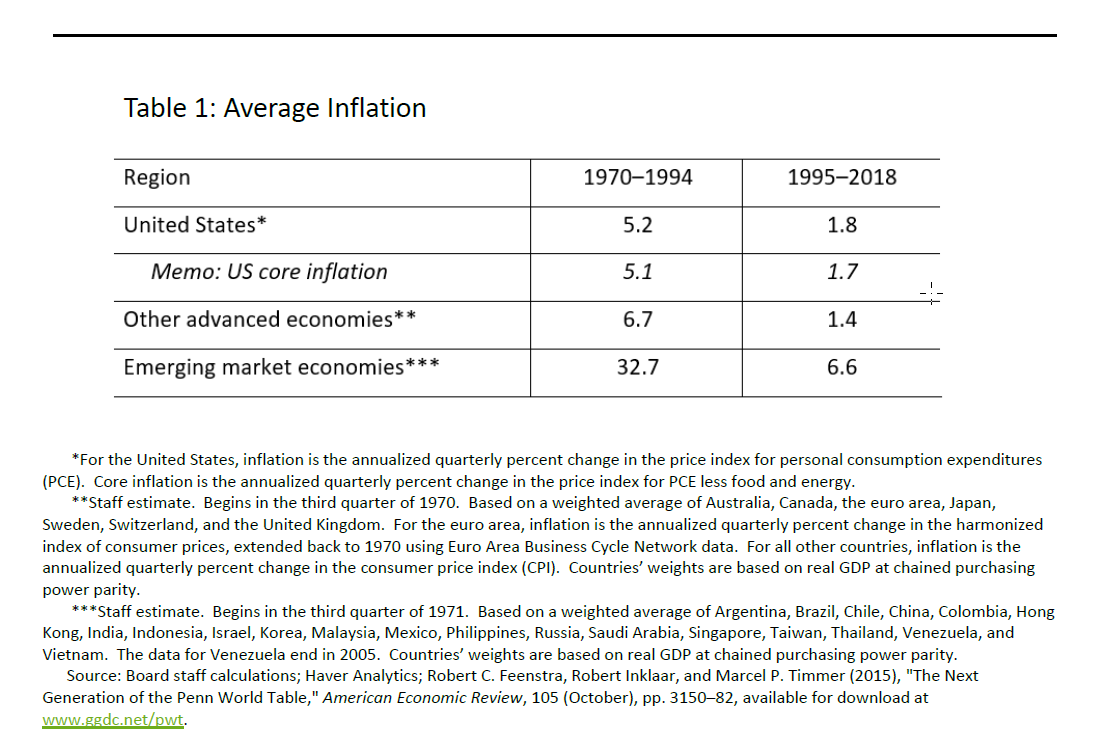

In addition to the decline in r* around the world, lower long-term bond yields also reflect the influence of the initial downshift and ultimate anchoring of inflation expectations in many countries after the mid-1990s. Unlike the decline in r*, which primarily reflects fundamental “real” factors that are outside the control of a central bank, the decline and ultimate anchoring of inflation and inflation expectations in both major and many emerging economies were the direct consequence of the widespread adoption and commitment to transparent, flexible inflation-targeting monetary policy strategies. For example, in the United States, after the collapse of Bretton Woods, inflation spiraled upward, hitting double-digit rates in the 1970s and early 1980s. But by the mid-1980s, the back of inflation had been broken (thank you, Paul Volcker), and total personal consumption expenditure (PCE) inflation averaged less than 4 percent from 1985 to 1990. Following the 1990–91 recession, inflation fell further, and, by the mid-1990s, the conditions for price stability in the United States had been achieved (thank you, Alan Greenspan). From the mid-1990s until the Great Recession, U.S. PCE inflation averaged about 2 percent. And, of course, this step-down in inflation has been global, with the other major advanced economies experiencing a similar shift down (table 1, “Average Inflation Rates”). Many major emerging market economies as well have seen a remarkable and very welcome decline in average inflation rates as a result of adopting and delivering on credible inflation-targeting polices. To the extent that the step-down in inflation is expected to persist, which appears to be the case, long-term yields have reflected this decline one-for-one.

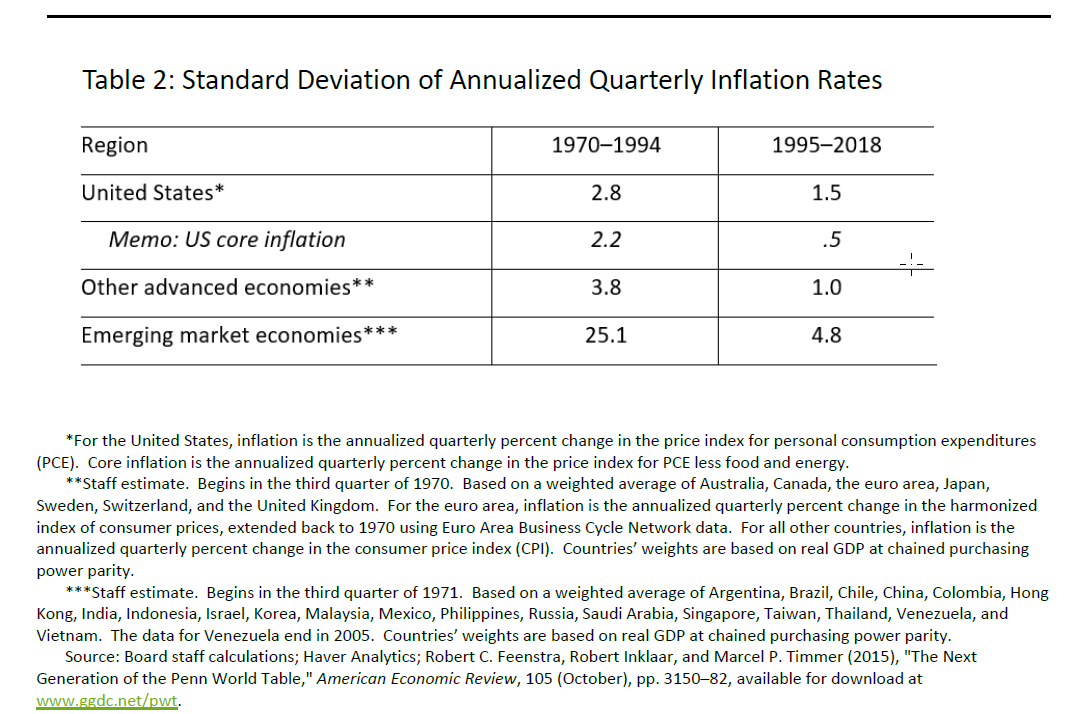

However, not only has the average level of inflation fallen, but inflation has also become more stable. After considerable volatility in the 1970s and 1980s, over the past few decades, inflation—especially core inflation, which excludes volatile food and energy prices—has, with rare exceptions, moved only within a relatively narrow range in many countries despite significant swings in the prices of oil and other commodities, recessions, the Global Financial Crisis, and unprecedented monetary policy actions. Reflecting this, inflation volatility, as measured by the standard deviation in quarterly inflation rates, has declined. (See table 2, “Standard Deviation of Annualized Quarterly Headline Inflation Rates.”)

What has been behind this global decline in inflation volatility? I would argue, as have many others, that monetary policy played a key role in reducing not only the average rate of inflation, but also the volatility of inflation.7 Inflation-targeting monetary policy can plausibly influence the variance of inflation through several channels. For example, in a textbook DSGE (dynamic stochastic general equilibrium) model (Clarida, Galí, and Gertler (CGG), 1999) featuring a central bank that implements policy via a Taylor-type rule, the equilibrium variance of inflation will be lower the more aggressively the central bank leans against exogenous shocks that push inflation away from target. So even if the variance of inflation shocks is constant, the variance of inflation itself will be an endogenous function of monetary policy. Another related channel through which monetary policy can influence the variance of inflation is by changing the equilibrium persistence of inflation deviations from target. In the textbook CGG model (1999), augmented with a hybrid Phillips curve that features an inertial backward-looking component, the equilibrium persistence of inflation is an endogenous function of the monetary policy rule such that the more aggressively the central bank leans against exogenous shocks that push inflation away from target, the less persistent are inflation deviations from target in equilibrium. In the simple case in which equilibrium inflation is a first-order autoregressive process (as it is in the CGG (1999) model under optimal policy), the equilibrium unconditional variance of inflation is monotonic in inflation persistence for any given constant variance of inflation shocks. Of course, non-monetary factors may also have contributed to a lower variance of inflation. For example, the variance of underlying exogenous shocks to aggregate supply and demand may have fortuitously and coincidentally fallen in tandem with the adoption of inflation targeting in many countries.

I will now turn to a third factor behind the decline in global bond yields, the decline in term premiums that is estimated to have occurred in many countries over the past 20 years. Most studies find that term premiums have fallen substantially in major economies over the past 20 years, and that in the United States term premiums may have been negative for some time. Decomposing the factors that drive equilibrium term premiums is an active area of academic research, and I will not attempt to summarize or synthesize this vast literature.8 But I would like to emphasize what seems to me to be three contributors to the decline in the term premium in the United States and perhaps in other countries as well.9

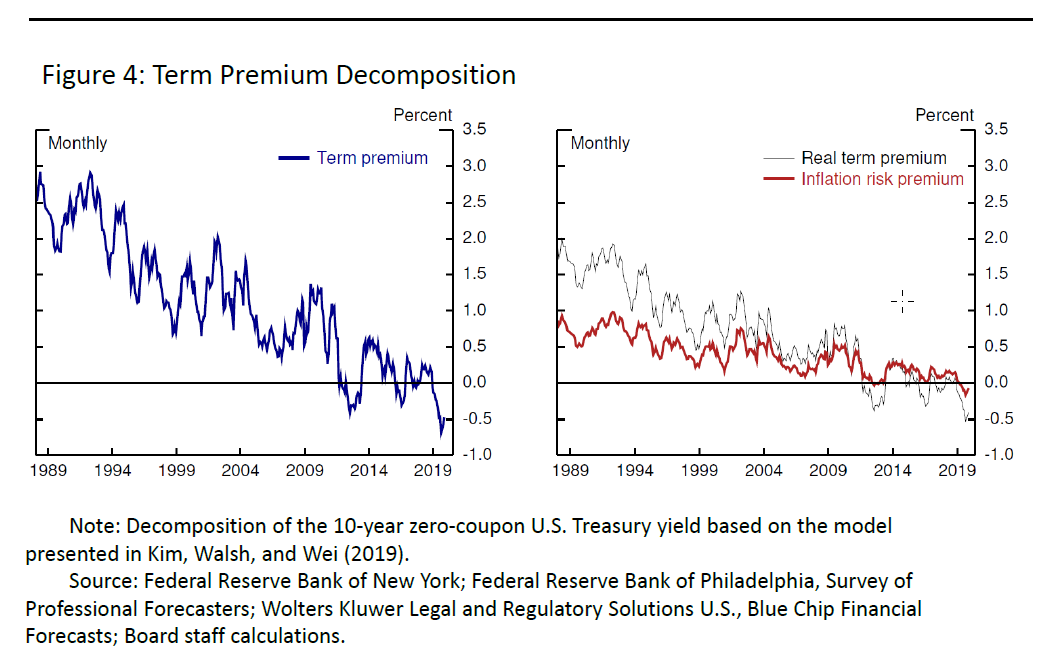

First, the decline in inflation volatility has almost certainly been important in driving the term premium on nominal bonds lower. The real ex-post payoff from holding a nominal bond to maturity is directly exposed to price-level risk, and thus, all else being equal, a decline in inflation volatility makes the real purchasing power of the bond’s payoff less risky. Through this channel, the decline in inflation volatility should be reflected in a smaller inflation risk premium in nominal bond yields, which is exactly what is estimated in the Kim, Walsh, and Wei (2019) yield curve model (figure 4, “Term Premium Decomposition”). Indeed, this yield curve model attributes around 100 basis points of the decline in the U.S. 10-year nominal term premium since the early 1990s to a decline in the inflation risk premium.

A second likely contributor to the decline in the U.S. term premium over the past decade is the Federal Reserve’s substantial purchases of long-duration Treasury securities and mortgage-backed securities in three large-scale asset purchase (LSAP) programs and one maturity extension program between late 2008 and late 2014. These purchases, which were concentrated at the longer end of the U.S. yield curve, took duration out of the market and thus lowered the equilibrium yield required by investors to hold the reduced supply of long-duration assets instead of holding and rolling over short-maturity Treasury bills. Estimates of the cumulative effect of these purchases on the U.S. term premium span a wide range, with some estimates above 100 basis points.10 Moreover, the global market for sovereign bonds and currency-hedged duration is tightly integrated, and it seems likely that asset purchase programs in other major economies, such as Japan, the euro area, and the United Kingdom, have contributed as well to reducing the term premium in Treasury securities (and, of course, LSAP programs in the United States likely contributed to lower term premiums abroad).

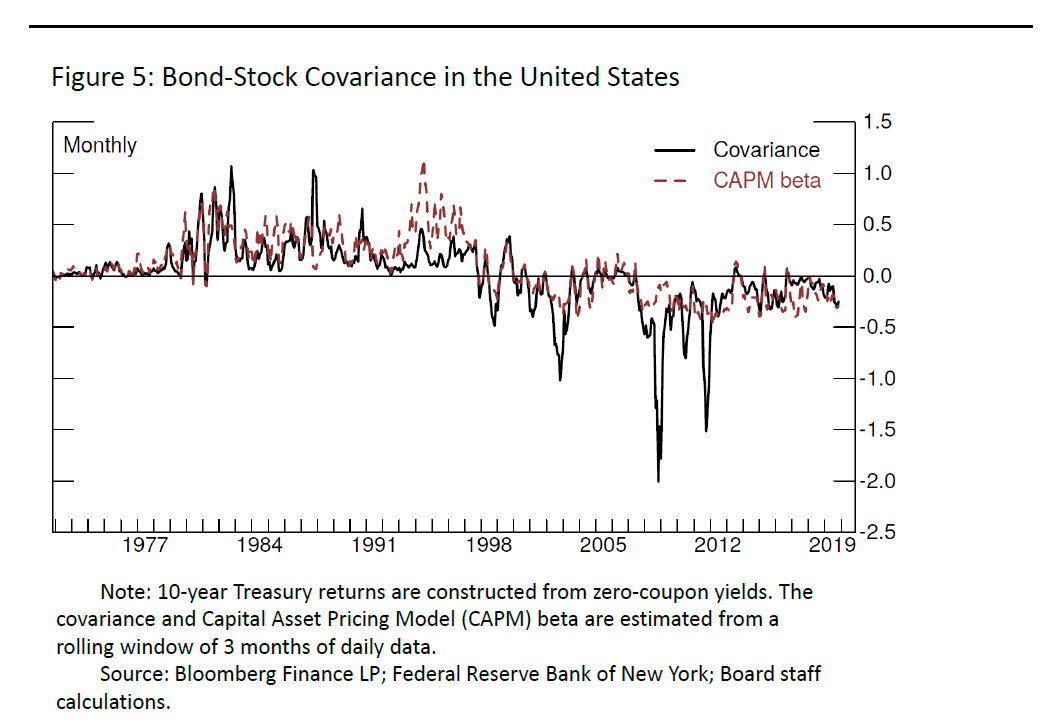

A third contributor to a lower U.S. term premium is much less widely appreciated than lower inflation volatility and LSAPs. This reflects the value that bonds have provided over the past 20 years as a hedge against equity risk. As documented by Campbell, Sunderam, and Viceira (CSV) (2017) and Campbell, Pflueger, and Viceira (CPV) (forthcoming), the empirical correlation between U.S. bond and stock returns changed sign in the late 1990s from positive to negative (figure 5, “Bond–Stock Covariance in the United States”). In the 1970s and 1980s, the sign of the correlation was positive, which implies that bond and stock returns tended to rise and fall together. In this period, bonds provided a diversification benefit when added to an equity portfolio (the bond return beta to stocks averaged 0.2) but not a hedge against equity risk. Since the late 1990s, the empirical correlation between bond and stock returns has typically been negative (the bond return beta to stocks has averaged negative 0.2). This means that since the late 1990s, bond returns tend to be high and positive when stock returns are low and negative so that nominal bonds have been a valuable outright hedge against equity risk. As such, we would expect the equilibrium yield on bonds to be lower than otherwise, as investors should bid up their price to reflect their value as a hedge against equity risk (relative to their value when the bond beta to stocks was positive). According to CSV, the hedging value of nominal bonds with a negative beta to stocks could substantially lower the equilibrium term premium on bonds. Quoting from their paper (page 265),

“Thus from peak to trough, the realized beta of Treasury bonds has declined by about 0.6 and has changed sign. According to the CAPM [capital asset pricing model], this would imply that term premia on 10-year zero-coupon Treasuries should have declined by 60 percent of the equity premium.”11

As a concrete example, consider the (ex-post) hedging value of bonds for equity risk in the Global Financial Crisis. In 2008, the total return on the S&P 500 index was around minus 37 percent, while the total return of the on-the-run 30-year Treasury bond was about 38 percent!

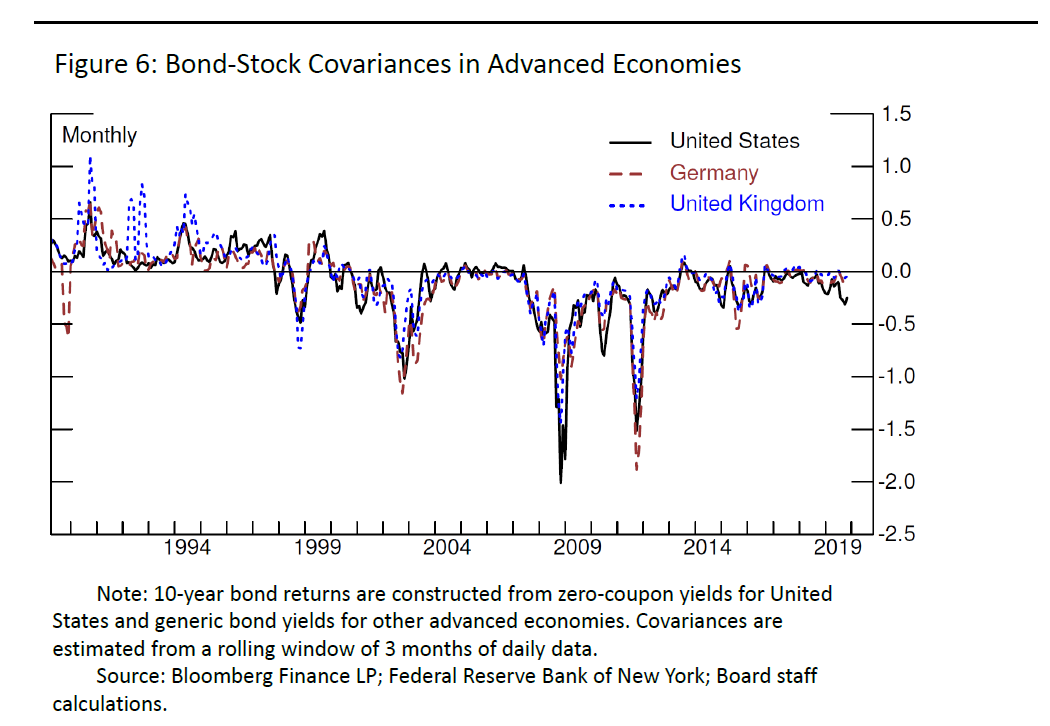

There is likely no single explanation for the change in sign of the correlation between equilibrium bond and stock returns in the United States and in other major countries (figure 6, “Bond–Stock Covariances in Advanced Economies”).12 One recent paper that does rigorously model the changing value of bonds for hedging equity risk is by CPV. This paper develops and estimates a habit persistence consumption asset pricing model in which the sign of the equilibrium covariance between equity and bond returns depends on the reduced-form correlation between inflation and the output gap, the correlation between the federal funds rate and the output gap, as well as the equilibrium persistence of inflation. CPV document in U.S. data, for a sample spanning 1979:Q3 to 2011:Q4, that (1) the correlation between inflation and the output gap changed sign from negative to positive; that (2) the correlation between the federal funds rate and the output gap changed sign, also from negative to positive; and that (3) the evidence of the sign change becomes statistically significant beginning in the late 1990s. CPV also document that the transitory component of inflation becomes much less persistent after the estimated break in their sample.

The CPV paper is agnostic as to why the reduced-form correlation between inflation and the output gap and that between the federal funds rate and the output gap both change sign in their sample, but the authors do demonstrate that in their asset pricing model, these reduced-form sign changes are sufficient to generate the sign change in the correlation between equity and bond returns that we observe in the data.

I, myself, believe that the change in the U.S. monetary policy regime that began in 1979 under Paul Volcker and that was extended by Alan Greenspan in the 1990s very likely contributed to the change in the sign of the correlation between inflation and the output gap as well as the change in sign of the correlation between the federal funds rate and the output gap that we observe in the data (Clarida, Galí, and Gertler, 2000). These are the sorts of patterns that a simple model of optimal monetary policy would produce when starting from an initial condition in which inflation is well above the (implicit) target, as was the case in 1979. High initial inflation triggers a policy response for the central bank to push up the real policy rate well above inflation in order to push output below potential, which, via the Phillips curve, will, over time, lower inflation toward the target. If this policy succeeds ex post, inflation expectations become anchored at the new lower level of inflation, and policy can, then, respond to demand shocks by adjusting real rates pro-cyclically, the opposite of what is required when initial inflation is too high and inflation expectations are not anchored.13 Inflation will also be pro-cyclical with well-anchored inflation expectations if demand shocks dominate and inflation expectations remain anchored.

Implications for Monetary Policy: The Federal Reserve’s Framework Review

By lowering expected inflation, by anchoring expected inflation at a low level, by contributing to a reduction in the volatility of inflation—and thus a reduction in the inflation risk premium—and by contributing to creating a hedging value of long-duration sovereign bonds, inflation-targeting monetary policy has lowered equilibrium bond yields relative to equilibrium short rates substantially compared with the experience of the 1970s and early 1980s. But, as I noted earlier, during the past decade equilibrium short rates have themselves also fallen substantially. These two phenomena, taken together, have resulted in sovereign bond yields that are substantially lower than the pre-crisis experience and thus substantially closer to the effective lower bound for the policy rate than they were before the crisis. But what does this mean for monetary policy? At its most basic level, the answer to this question could depend on how far the nominal policy rate is from the effective lower bound (ELB) and the extent to which the term premium on long-duration bonds can become even more negative than it is at present (at least in the United States).14 While I do not have a precise answer to this question, I will confess that I think it highly unlikely in the next downturn, whenever it is, that 10-year U.S. Treasury yields will fall by the roughly 390 basis points that we observed between June 2007 and July 2016 (the bottom in Treasury yields in this cycle) or even decline by the roughly 360 basis points that we observed between January 2000 and June 2003.

The reality of low neutral rates and equilibrium bond yields has motivated us at the Federal Reserve to take a hard look this year at our monetary policy strategy, tools, and communication practices. While we believe our existing framework, in place since 2012, has served us well, we believe now is a good time to step back and assess whether, and in what possible ways, we can refine our strategy, tools, and communication practices to achieve and maintain our goals as consistently and robustly as possible in the world we live in today.15 As I have noted before, the review of our current framework is wide ranging, and we are not prejudging where it will take us, but events of the past decade highlight three broad questions that we will seek to answer with our review.

The first question is, “Can the Federal Reserve best meet its statutory objectives with its existing monetary policy strategy, or should it consider strategies that aim to reverse past misses of the inflation objective?” Central banks are generally believed to have effective tools for preventing persistent inflation overshoots. But persistent inflation shortfalls, such as those associated with the ELB, carry the risk that longer-term inflation expectations become anchored below the stated inflation goal.16 At our September Federal Open Market Committee (FOMC) meeting, we discussed options for mitigating ELB risks, including “makeup” strategies in which policymakers would promise to make up for past inflation shortfalls with a sustained accommodative stance of policy intended to generate higher future inflation.17 Such strategies provide accommodation at the ELB by keeping the policy rate low for an extended period. Makeup strategies may also help anchor inflation expectations more firmly at 2 percent than would a policy strategy that does not compensate for past inflation misses. But the benefits of makeup strategies depend importantly on the private sector’s understanding of them as well as the belief that future policymakers will follow through on promises to keep policy accommodative. An advantage of our current framework over makeup approaches is that it has provided the Committee with the flexibility to assess a broad range of factors and information in choosing its policy actions, and these actions can vary depending on economic circumstances in order to best achieve our dual-mandate goals.

We are also considering whether our existing monetary policy tools are adequate to achieve and maintain maximum employment and price stability, or whether our toolkit should be expanded and, if so, how. Because the U.S. economy required additional support after the ELB was reached in 2008, the FOMC deployed two additional tools beyond changes to the target for the federal funds rate: balance sheet policies and forward guidance about the likely path of the federal funds rate.18 The review is examining the efficacy of these existing tools, as well as additional tools for easing policy when the ELB is binding, in light of the more recent experiences of other economies.

Finally, we are focusing on how the FOMC can improve the communication of its policy framework and actions. Our communication practices have evolved considerably since 1994, when the Federal Reserve released the first statement after an FOMC meeting.19 As part of the review, we are assessing the Committee’s current and past communications and additional forms of communication that could be helpful.

In terms of process, we have heard from a broad range of interested individuals and groups in 14 Fed Listens events this year. At our July 2019 FOMC meeting, the Committee began to assess what we have learned from these events and to receive briefings from System staff on topics relevant to the review.20 But we still have much to discuss at upcoming meetings. We will share our findings with the public when we have completed our review, likely during the first half of 2020.

Concluding Remarks

The economy is constantly evolving, bringing with it new opportunities and challenges. One of these challenges is how best to conduct monetary policy in the new world of low equilibrium interest rates. It makes sense for us to remain open minded as we assess current practices and consider ideas that could potentially enhance our ability to deliver on the goals the Congress has assigned us. For this reason, my colleagues and I do not want to preempt or to predict our ultimate findings. What I can say is that any refinements or more material changes to our framework that we might make will be aimed solely at enhancing our ability to achieve and sustain our dual-mandate objectives in the world we live in today.

Stepping back, earlier today, speakers at this conference discussed the challenges of making monetary policy in an uncertain and risky environment. In my remarks, I have laid out an important example of the interaction of the macroeconomy, monetary policy, and the market response to risk. The papers you are about to discuss throughout the next two days present cutting-edge esearch on the effect and measurement of risk and uncertainty and volatility, with a special focus on monetary policy and market behavior. As someone on the front lines, I look forward to learning from your insights and encourage your rich discussion over the next few days and your continued work on how to make my job easier! Thank you, and good luck!

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}