With the first half of 2020 in the books and Q2 earnings season upon us once again, the trading industry braces for earnings shocks and forward guidance as well as for the stock trading environment of the second half of the year. The COVID-19 impact is likely to be more severe in Q2, according to Giles Coghlan, Chief Currency Analyst at HYCM.

For reasons that are now obvious to almost everyone, markets were broadly expecting Q1 to be a bad quarter for company earnings. However, it was Q2 that was expected to bear the brunt of the economic cost of COVID-19. Many companies withheld forward EPS guidance in Q1 due to the pandemic, so aside from the pains associated with reopening the economy this coming earnings season may also have a few surprises in store. According to FactSet, of the 48 companies that did provide forward EPS guidance for Q2, 27 issued negative guidance and only 21 issued positive guidance. Additionally, we saw a slew of downward revisions in the relatively few companies that did provide forward guidance at the end of Q1″, Coghlan explained.

If the forecasts hold true, total earnings for the S&P 500 are expected to fall by more than 40% in Q2, with a decline in revenues in excess of 11%, making it the largest reported year-over-year decline since Q4 of 2008. Earnings declines in the automotive sector, transportation and energy, are expected in the triple digits. These are the hardest hit.

If the forecasts hold true, total earnings for the S&P 500 are expected to fall by more than 40% in Q2, with a decline in revenues in excess of 11%, making it the largest reported year-over-year decline since Q4 of 2008. Earnings declines in the automotive sector, transportation and energy, are expected in the triple digits. These are the hardest hit.

On the bright side are the technology sector, with Apple, Amazon, Facebook, and Microsoft having reclaimed their former all.time highs. Despite this, the broader tech sector is still expected to incur losses, albeit more modest ones, with revenues expected to come in around 1% lower and earnings around 13% lower than this time last year. Healthcare and utilities are the only two sectors expected to record year-over-year revenue growth, with revenues up by 0.7% and 0.2%, respectively.

According to the HYCM analyst, the US stock market will not recover fully until 2021. “At the end of March, estimated revenue declines for Q2 of 2020 were forecasted at -1.6%. As we have seen above, the actual figures today are around -11%, which reveals the kind of climate we currently find ourselves in, as well as the difficulty in predicting a situation with so many unknown variables”, Coghlan added. “The earnings estimates for Q3 and Q4 of this year currently stand at around -25% and -13% respectively, with an expected return to earnings growth anticipated in Q1 of 2021. Whether 2021’s figures are to reveal growth when compared to 2019 (and indeed whether 2020s Q3 and Q4 forecasts aren’t as wildly off as Q2’s has been) depends largely on whether the reopening of the US economy goes as planned. This means no second wave of infections requiring a reappraisal of reopening policies or even, in a worst-case scenario, a selective return to lockdown for certain states.”

According to the HYCM analyst, the US stock market will not recover fully until 2021. “At the end of March, estimated revenue declines for Q2 of 2020 were forecasted at -1.6%. As we have seen above, the actual figures today are around -11%, which reveals the kind of climate we currently find ourselves in, as well as the difficulty in predicting a situation with so many unknown variables”, Coghlan added. “The earnings estimates for Q3 and Q4 of this year currently stand at around -25% and -13% respectively, with an expected return to earnings growth anticipated in Q1 of 2021. Whether 2021’s figures are to reveal growth when compared to 2019 (and indeed whether 2020s Q3 and Q4 forecasts aren’t as wildly off as Q2’s has been) depends largely on whether the reopening of the US economy goes as planned. This means no second wave of infections requiring a reappraisal of reopening policies or even, in a worst-case scenario, a selective return to lockdown for certain states.”

Dip-buying has been buoying US markets, but the HYCM analyst says this may be unwarranted at this time, despite the Federal Reserve’s incredible amounts of stimulus, which has effectively muddied price discovery across almost all asset classes.

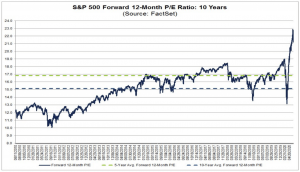

“Relative to the state of the real economy, by most measures US stocks are currently overpriced. When you look at the forward 12-month P/E ratios, the S&P 500 is currently trading at more than 21 times earnings, which is significantly higher than both its 5-year (16.8) and 10-year (15.1) averages. Since the market turbulence of Q1, the price of the S&P 500 has risen by more than 16%, while its forward 12-month EPS estimate has fallen by over 13%. This leaves specific sectors of the index, and more importantly, individual stocks, ripe for a shake-up in the coming months”, Coghlan wrote.

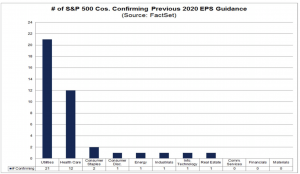

Aside from a general feeling that US stocks are overpriced, the HYCM analyst expects the Q2’s earnings season to come down to separating the stocks that have bounced too aggressively, from the ones that may not have bounced aggressively enough. “For instance, it’s no secret that tech has led the bounce we’ve seen recently. With P/E ratios currently at multi-year highs, you have to wonder whether some of these companies, great as they may be, could be looking at corrective moves”, Coghlan continued. “On the other hand, the utility and health sectors, which we’ve already discussed above, don’t seem to have been given the bump they deserve. The disparity between the number of

companies belonging to these sectors that have actually managed to meet their 2020 forward guidance targets (provided pre-coronavirus) is impressive. This is particularly true of utilities, which have seen a year-to-date decline of over 9%, while the broader S&P 500 index has seen a year-to-date increase of around 7%.”

The financial sector recorded the fourth largest downward revision in expected earnings since the beginning of the quarter, from around -14% to over -50%, and is currently lagging behind most other sectors. “This leaves the financial sector in an interesting situation. If history is anything to go by, it’s likely to be one of the main benefactors of the Fed’s outsized stimulus package. Perhaps it may be a little early for this influx of capital to register on the price of some of the main players in this sector; however, it’s possible that

we’ll see a bump in their performance as the benefits of all this “free” money begin to be felt”, Coghlan concluded.

HYCM is a retail FX and CFD broker founded in 1977, operating in Asia, Europe, and the Middle East. It is regulated by the FCA and CySEC and CIMA and represented globally in the United Kingdom, Hong Kong, Cyprus and Dubai.