The previous week witnessed a momentary spike in the DXY index, briefly surpassing the 105-level mark. However, any prospects of a sustained upswing were swiftly quashed as the US dollar continued its downward trend, despite the positive Non-Farm Payroll (NFP) report, which boasted a commendable 303k job addition.

This reluctance to embrace the greenback raises a pertinent question: What factors are contributing to the hesitancy in USD acquisition? While it may be premature to declare a definitive turning point, several factors contribute to this narrative.

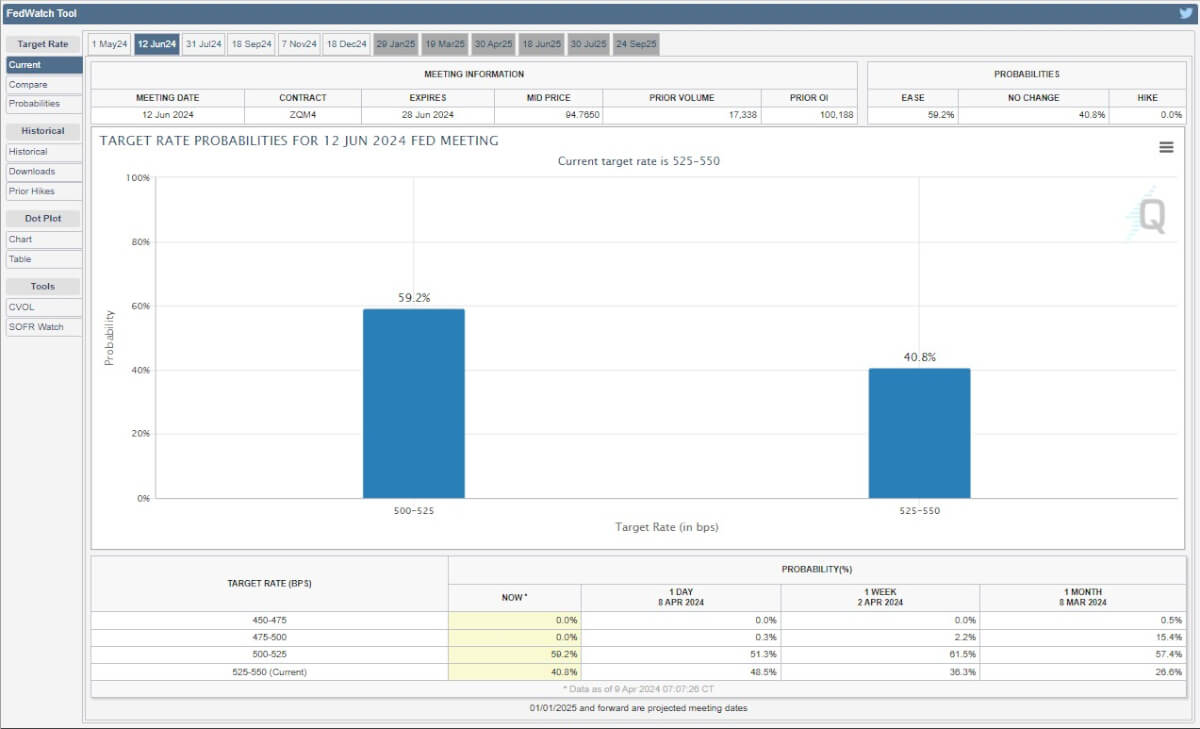

Certainly, the recent release of Consumer Price Index (CPI) data has raised doubts. Following two consecutive positive surprises, concerns linger over a potential downturn, which could revive expectations of a rate cut as early as June. However, reservations towards dollar acquisition extend beyond impending economic data. Market participants harbor scepticism, particularly regarding the reliability of the NFP figures. There is a notable disparity between the household survey and the establishment survey regarding employment metrics. While the establishment survey tallies job creation, the household survey accounts for individuals employed, failing to capture those with multiple jobs. The increase in part-time employment juxtaposed with a decline in full-time positions highlights this inconsistency.

FedWatch Tool

Moreover, indicators such as the ISM employment indices and the NFIB hiring index paint a less optimistic picture of the employment landscape, raising doubts about the sustained strength of the NFP data. The slowdown in average hourly earnings growth supports the notion that part-time employment plays a significant role. However, despite these reservations, the surge in US yields post-NFP fails to elicit a proportional increase in USD demand.

Another factor contributing to the diminishing appeal of the dollar could be the growing signs of economic recovery in Europe. Strong industrial production figures from Germany and optimistic sentiment indices suggest a positive outlook for the Euro and Pound Sterling, thereby reducing the attractiveness of the dollar. The resurgence of European economies, bouncing back from the turmoil of energy price shocks, serves as a significant counterbalance to USD appreciation.

In contrast, the semi-annual report on monetary policy delivered by BoJ Governor Ueda barely registers any notable impact on the Japanese Yen. Emphasizing the persistent challenge of low inflation and hinting at a cautious approach to further monetary tightening, Governor Ueda’s remarks maintain a neutral tone. While the possibility of FX intervention by the BoJ looms if yen movements threaten inflation, the overall sentiment suggests a cautious approach.

In conclusion, as the USD struggles with tepid demand amid lingering doubts over economic data and robust European growth, the JPY remains entrenched in a cautious monetary policy stance. The trajectory of both currencies’ hinges on the interplay of economic indicators and central bank actions, shaping the dynamics of the global forex market.

Disclaimer: The subject matter and the content of this article are solely the views of the author. FinanceFeeds does not bear any legal responsibility for the content of this article and they do not reflect the viewpoint of FinanceFeeds or its editorial staff.