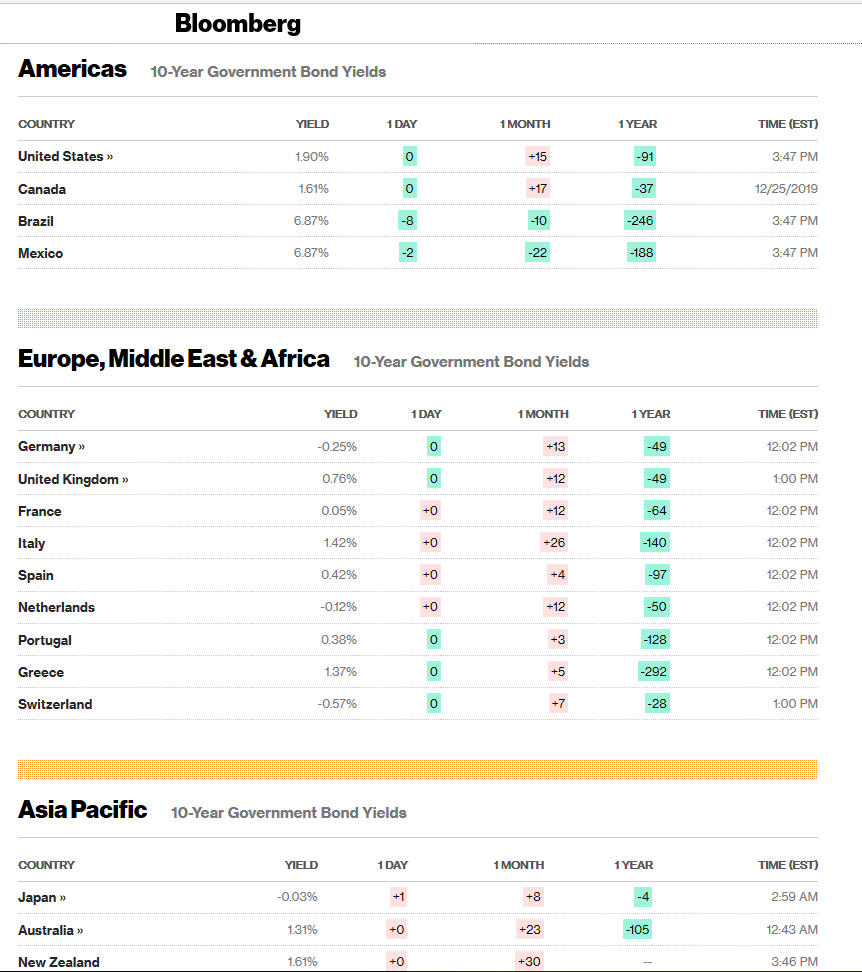

Summary: The Dollar Index (USD/DXY) a popular gauge of the Greenback’s value against a basket of foreign currencies dipped 0.12% to 97.523 (97.660) in thin, holiday affected trade. Most markets were closed on Christmas Day with seven centres still closed yesterday. US Bond Yields slipped following a mediocre treasury auction affected by low volumes. The 7-Year bond yield retreated to 1.83% from 1.842%. Benchmark Ten-Year US notes slipped to 1.90% (1.93% on Dec. 24). Optimism buoyed the thin markets as China and US prepared to go through the necessary procedures before signing their phase 1 trade deal. Resource currencies outperformed with the Australian Dollar lifting to 0.69464 (0.6923), fresh 3-month highs. The Kiwi rallied 0.40% to 0.6670 (0.6637) while the US Dollar fell against Canada’s Loonie to 1.3107 (1.3150). The Euro was up 0.09% to 1.1105 (1.1093). Sterling recovered to 1.3005 (1.2935) against the overall weaker US Dollar. Wall Street equities extended their winning streak, led by a rally in technology stocks which boosted the US NASDAQ up 0.6%. The S&P 500 gained 0.3% to 3,239 (3,227).

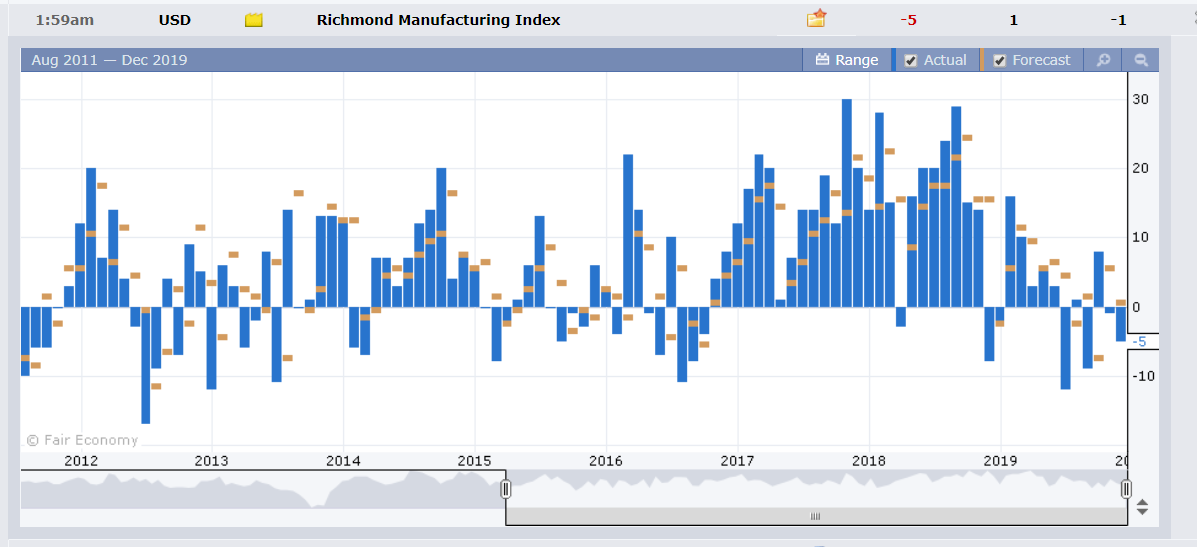

A set of weaker than expected US economic reports weighed on the Dollar. US Headline and Core Durable Goods Orders both underwhelmed. Core Durable Goods Orders fell to -2.0%, widely missing forecasts of a 1.5% gain. US New Home Sales dipped to 719,000 units (vs forecasts of 730,000). US Richmond Manufacturing Index dipped in December to -5 from the previous month’s -1, missing forecasts of 1. Japan’s Annual Housing Starts underwhelmed, falling 12.7%, against expectations of a 7.9% fall. US Weekly Unemployment Claims matched the previous report with 222,000.

- AUD/USD – The Aussie Battler gained 0.35% to 0.6945 (NY close) on the rally in trade sensitive currencies and the weaker US Dollar. The Australian Dollar hit 3-month highs at 0.6946 in New York. This morning AUD/USD hit 0.69496, a near five-month peak in early Sydney before easing to settle at 0.6943 currently.

- USD/DXY – The Dollar Index dipped to 97.523 from 97.66 (December 24) following a weaker set of US economic data of late. The Dollar Index hit a high earlier this week at 97.758 following the upbeat US Q3 GDP report.

- EUR/USD – The Euro climbed back above to 1.1100 level to finish at 1.1107 in New York. The shared currency dipped to 1.10663 at the start of the week. Overnight high traded was 1.11090.

- GBP/USD – The British Pound recovered to 1.3007 following its slump to a low at 1.29044 on Tuesday. Overall US Dollar weakness provided Sterling support which is still a long way below its December 13 top at 1.3514.

On the Lookout: Expect thin trading conditions to continue dominated FX in Asia ahead of the weekend and year-end. Today sees a data dump from Japan which could move the Yen. Apart from the Japanese reports, economic data elsewhere are scarce. The European Central Bank releases its Economic Bulletin, which will provide traders with more clues from the ECB on the economic future of Europe. Switzerland sees Credit Suisse’s Economic Expectations Survey (a survey of 30 investors and analysts). Finally, the UK releases its High Street Lending report.

Trading Perspective: FX liquidity will remain at a premium, traders will be content to stick with the recently established ranges. The drop in US bond yields were not matched by its global rivals and this will weigh on the Dollar Index. Markets will be watching the headlines for a confirmation of the formal signing between China and the US of their phase 1 trade deal. If this happens, we should see more downside pressure on the US Dollar, with resource FX benefitting.

- EUR/USD – The Euro managed to climb above 1.1100 on the overall weaker US Dollar. Germany’s 10-year Bund yield was unchanged at -0.25% from December 24. EUR/USD closed at 1.1107 after trading to an overnight low at 1.10823. On the day, immediate support can be found at 1.1085 (overnight low 1.10823) followed by 1.1065. Look for consolidation today with a likely range of 1.1085-1.1125. Prefer to buy dips.

- AUD/USD – The Aussie Battler rose to 0.69496 in early Sydney boosted by trade optimism and an overall weaker Greenback. AUD/USD retreated to 0.6943 where it currently trades now. AUD/USD has immediate resistance at 0.6950 followed by 0.6980 then 0.7010. Immediate support can be found at 0.6925 (overnight low 0.69215) followed by 0.6900.

Look for consolidation in Asia today with a likely range at 0.6920-0.6950. Look to trade both sides. - USD/JPY – The Dollar traded within a 109.363 and 109.685 range overnight, closing at 109.57 where it currently sits. Overnight Japanese 10-year JGB yields were down 3 basis points to -0.03%, matching the fall of its US counterpart. USD/JPY has immediate resistance at 109.70 followed by 110.00 today. There is immediate support at 109.35 (overnight low 109.363) followed by 109.10. Japanese data dump today could see the currency move. An improved set of Japanese data will see the currency strengthen against its US counterpart. If data is worse than forecast, USD/JPY should rally. Look for consolidation first up between 109.35-109.65.

- GBP/USD – Sterling recovered from its lows earlier in the week to finish at 1.3007. Immediate support for the Pound lies at 1.2960 (overnight low) followed by 1.2935 and 1.2905. Immediate resistance can be found at 1.3020 (overnight high 1.30159) followed by 1.3060. There are no major UK events for today although the Pound is still shaky on the uncertainty of PM Boris Johnson’s Brexit plan. A rise in crude oil overnight supported the British currency. Look for a likely trading range today of 1.2985-1.3085. Prefer to buy on dips to 1.2960.

Happy trading and Friday all.